This week, the 25th City Food & Drink Lecture in The Guildhall, London, addresses the question “Can the food & drink industry make the next 25 years healthier than the last?”. If consumers could be convinced to eat (or drink) more fruit and veg. that’d be very helpful but we’ve got only a modest track record of success! Is this a British problem? Far from it. Per capita consumption of fresh fruit & veg. has slipped backwards in Australia, New Zealand, Canada and USA, amongst others. Across the entire fresh produce market, are all consumer age groups fruit & veg. slowpokes?:

children under-consume vegetables and have done so for decades (“don’t like to try/the taste of vegetables, not exciting/uncool”). There are encouraging initiatives such as VegPower in the UK and The Wiggles Yummy Yummy in Australia to redress the decline but it’s back-breakingly hard;

adults under 40-year-olds aren’t much better than the kids, shopping less frequently than their elder peers for fresh produce in supermarkets and are much more likely to demand their fruit & veg. in ready-to-eat snack and mini-meal form (smoothies, bowls, etc.);

even ageing “Boomers” (60+ years) are eating less reflecting that portion size tends to decline with age and on bitey produce there’s their teeth, of course! Mind you, we’ll miss them when they’re gone as, in Australia, 55+ year olds have a 40-50% greater fresh produce consumption than those younger.

Declining per capita consumption of fresh fruit & vegetables, particularly if it’s based on retail sales via supermarkets and traditional greengrocers, may seem worrisome, but this doesn’t capture total fruit and vegetable consumption which includes canned, frozen, dehydrated and fresh processed which are sold in regular and alternative retail outlets and alternative product forms. Three examples come to mind:

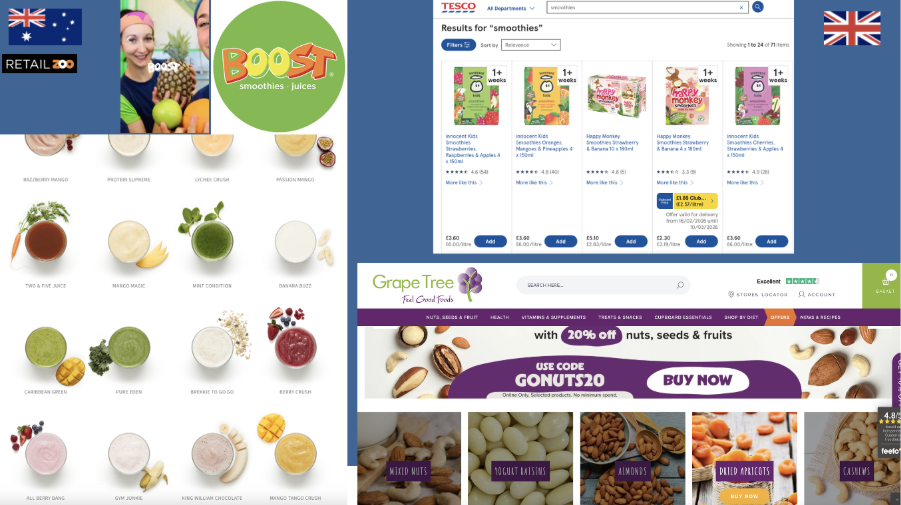

juices and smoothies festoon the retail shelves of our supermarkets. Click “Smoothies” on Tesco.Com and there are 71 choices and 195 if you click on “Juices”. The hugely popular “meal deals” invariably include a fruit/veg. snack or drink;

Boost Juice making fruit & veg. smoothies in 16 countries around the world (including Australia its “home”, New Zealand and UK);

and Grape Tree in the UK with close to 200 stores selling nuts, seeds, dried fruit and more at very competitive prices to the major grocery retailers.

Clarence Birdseye introduced the world to frozen peas 100 years ago and, if you eat broad beans, when did you last buy them fresh? Frozen products increasingly dominate the potato market globally (who makes chips/French fries from scratch?). A wide range of frozen field veg. prospered during the 1950/60s only to be beaten back in the UK as supermarkets extended their global procurement of fresh produce. Yet, frozen sales made a comeback through “lockdown” in the very early 2020s and blenders such as nutribullet take the labour out of breakfast smoothie-making from both fresh and frozen even for “I want it NOW” Gen. Z consumers! In New Zealand, frozen, dried or pickled produce are the only options during the domestic fruit & veg. off seasons as ALL fresh produce imports are banned.

Seven out of ten households in the UK, Australia and New Zealand have an air fryer (3rd most popular kitchen appliance after the toaster and microwave) popular because of speed of cooking and energy efficiency. Its arrival has boosted sales of frozen meat and vegetables, not least hard Winter vegetables like sweet potatoes, swede, squash and brassicas such as Brussels sprouts. Keep them in the freezer and there’s no worries about shelf life and product waste that we have with the fresh items.

For many households, the form of what food and when/where we eat it is principally about convenience (n.b. convenient: the state of being able to proceed without difficulty). A recent Horticulture Australia consumer survey concludes that the biggest barrier to increasing fruit & veg. consumption at home is “lack of time and energy”: “I don’t have the time to plan, shop and prepare more … vegetables”. It’s no different in UK or New Zealand. Clearly, the outlook for pre-prepared fruit and veg. products looks good. For frozen and chilled, fresh prepared there’s no or very little UPF (Ultra Processed Food) perceptual barrier. Just ensure the ingredient list is short and natural.

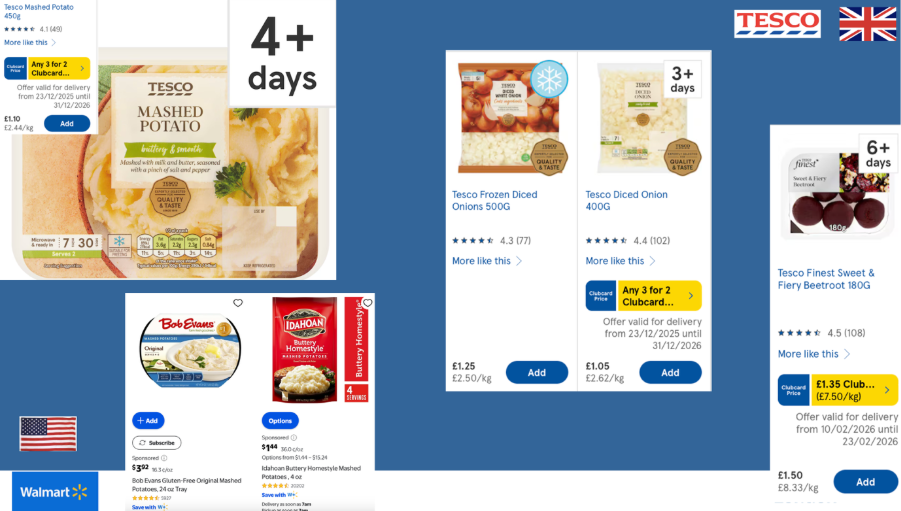

Keep an eye on the uptake of chilled ready mashed potatoes. NEVER in this household, you say! Well, maybe occasionally if I’m desperately short of time. Ooops, it’s become a routine purchase. The ingredients? Potatoes, milk, butter and a pinch of salt & pepper – not too scary! Tesco.Com has 20 mashed potato skus. Take a peek at Walmart’s offer in the USA. It has 720 mashed potato skus and, coincidentally, most are supplier branded, i.e. not supermarket own label. Onions are edging in the same direction – no more crying! We bet you haven’t boiled or pickled a beetroot in a decade.

Irrespective of whether fruit & vegetables are fresh whole/fresh prepared, frozen, pickled or whatever, 2 mega consumer trends are blowing a gale of consumer demand in our direction. First and gaining strength through the COVID period and up to this day is Gen. Z (under-30s) fuelling demand for healthy food products compared to older generations. Across the adult age ranges there are wellbeing concerns that recognise what we put in our tummies is an integral part of improving mental, physical and global environmental health. Second, there’s the anticipated impact that GLP-1s (Anti-Obesity Medication) is and will increasingly have on global diets as the medication moves towards pill form and at much lower prices. Early USA survey data shows that users feel better, eat less and eat healthier – bad news for the savoury and sweet snack sector, and for the fast-food sector as is, but very good news for those in the wider fruit and vegetable industry. After “clean” protein, fruit and veg. comes second on GLP-1 users must consume more list.

The future for the fruit and vegetable industry seems set fare. But …. as Gen. Z consumers drift into middle age and accumulate children, they just won’t develop an irresistible desire to prepare beef and Winter vegetable stews from scratch or yearn for difficult to peel citrus, even slicing melons may be challenging. Food and drink that is convenient will rule and convenient, to repeat, means I want it NOW! The notion of purchasing food ingredients will remain mysterious for most and they’ll seek meal components that they can bolt together into “a home cooked meal” or just buy the snack/mini/main meal in toto from a store or have Just Eat, Uber Eats or Grab (in Asia) deliver it. The implication of this for fresh produce producers and suppliers is that there will be another link in the chain between them and the consumer. Globally, the fresh produce industry is consolidating at speed. Expect to see the big players expand and cover all of the fruit & vegetable product formats – fresh, fresh prepared, frozen and more.

Finally, on health, we’ve talked before about how poor the fresh produce industry has been about communicating with consumers on the specific health attributes of their products. There are exceptions and Zespri comes to mind advising consumers that eating more kiwifruits will result in firmer, younger looking skin, and that kiwifruit Vitamin C levels knocks oranges into a cocked hat. Globally, consumers are seeking food with high fibre content. Shouldn’t this be, pardon the expression, one of our trump cards? Ask consumers in any survey “are fresh fruit and vegetables healthy for you and your family?” and they’ll nod with that “everyone knows that”. We need to be more specific as in “it’s good for …” and add in a health attribute that is important to them and for which we have genuine scientific research evidence.

Posted on 25th January 2026 by Prof. David Hughes & Miguel Flavian

The blog is back, returning to one of the hottest (and most enthusiastically argued-over) topics in the UK food and farming debate of the moment. We do recognise that many readers are busy, impatient and have a predilection to consume information via the phone whilst undertaking other tasks. As a result, we offer you: Option 1 – the “are you sitting comfortably with a bottle of wine?” version ; or Option 2 – “the cup of coffee and in a hurry” version. The latter is thanks to the summarising skills of ChatGPT and is waiting patiently for you at the end of the post.

The Bottle of Wine Version

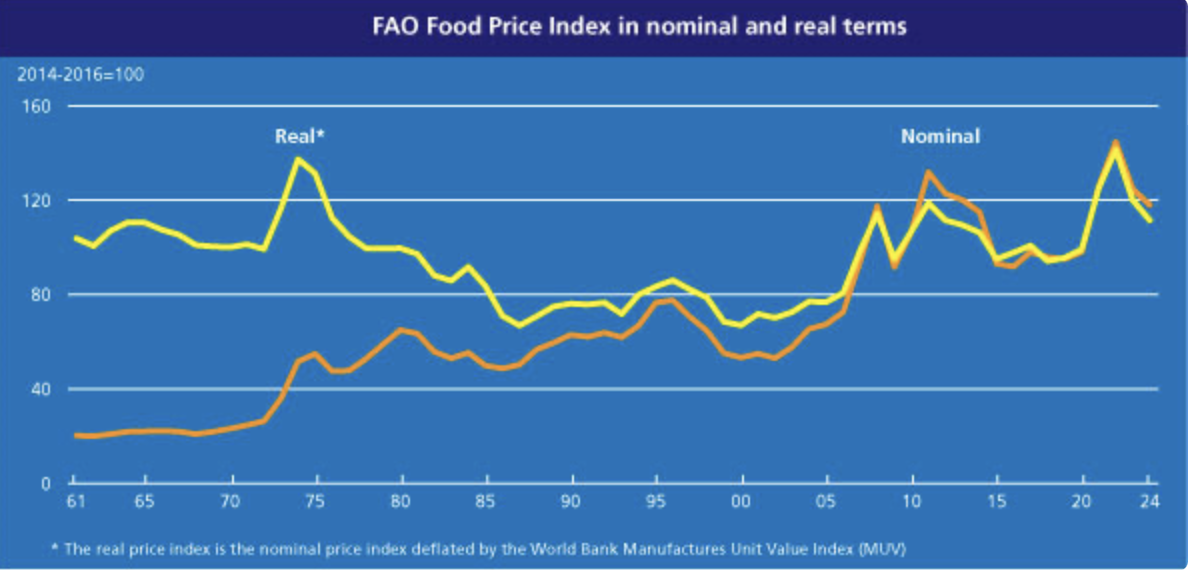

In December 2025, the FAO Global Food Price Index was 2% lower than a year earlier, hurrah! But, what’s vexing consumers is that global food prices are 31% higher than pre-Covid and most household incomes haven’t seen a similar rise. Good news for farmers? No, across the world many farmers are incandescent with rage as they’re buffeted by inflationary spikes in input costs, Trumpian tariff excesses, margin squeezes from more powerful supply chain “partners”, and extreme climate events. Concerns about national food security have bubbled to the top of the political agenda and are rife in the media with dark talk about the prospect of empty supermarket shelves for key foods.

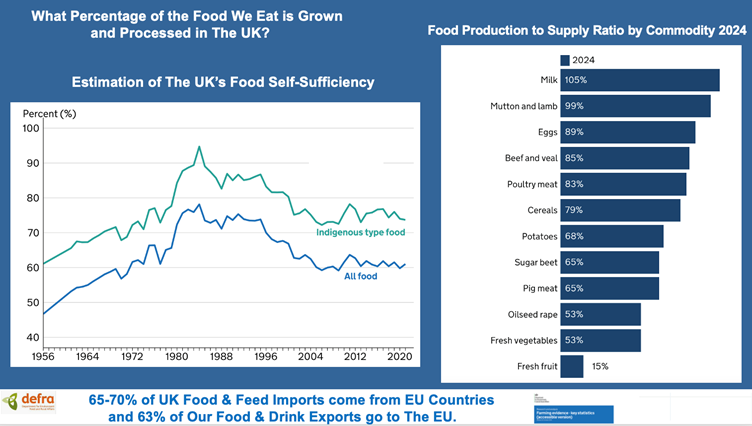

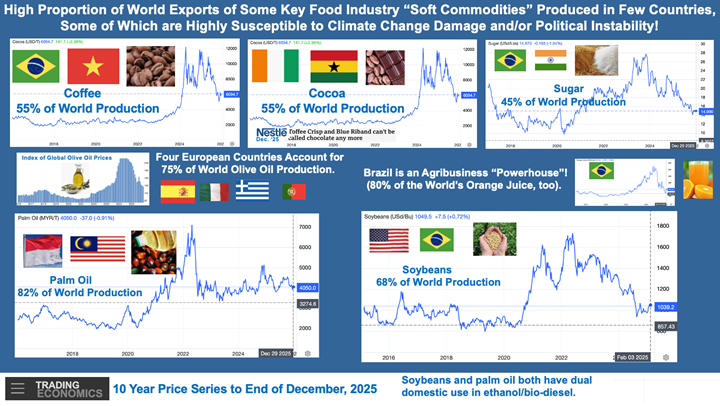

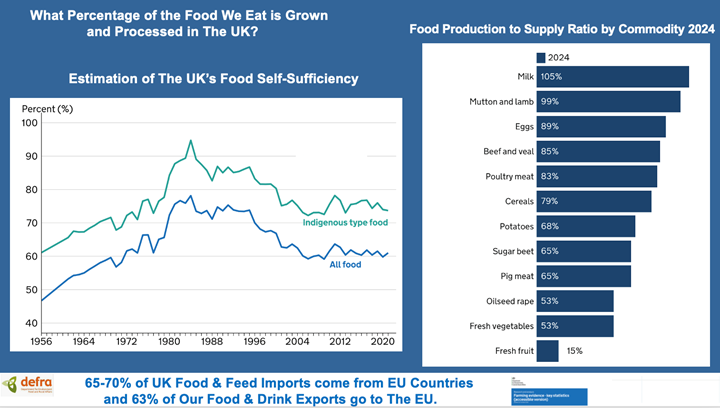

A high proportion of world exports of key food industry “soft commodities” are produced in few countries: e.g. coffee, cocoa, sugar, palm oil, olive oil, orange juice. If they have production problems, we have grocery procurement problems! At home and in history, UK food production was a shared job between our farmers and those offshore, largely from “The British Commonwealth”. UK food self-sufficiency was below 50% pre-WW2, rising to 75+% in our earlier EU years in the 1980’s, then, drifted down to settle around 60% in the 2000’s. In her Farming Profitability Review (December 2025), Minette Batters sees one of the routes to improve profitability of British farming and to increase our food self-sufficiency is through growing the British food & drink brand at home and abroad by “growing, making, producing and selling more from our farms….”. Food production expansion may be a key element in our national farming and food strategy but begs the question why are we only 60% self-sufficient in food now? Each of the principal commodity areas have their own explanatory tales:

milk and mutton & lamb – these were shared production duties with New Zealand, whereas beef in early years was principally British and supplemented by Argentina and Uruguay (remember cans of corned beef? Fray Bentos is a city in Uruguay!). Latterly, Irish beef has been commonplace in our market. What’s surprising is that the UK, uncommonly good at growing grass, didn’t emerge as a significant milk product and red meat exporter;

we’re good at poultry but, also, significant importers of chicken. Don’t look at the supermarket meat aisles for chilled imported chicken because that’s where the UK product is located. Most of the imported chicken, from inter alia Thailand, Poland, Ukraine, China, emerges in our market as the raw material for nuggets and kebabs sold, not least, via food service – “fast” chicken the default takeaway!;

sugar was a shared job with our Caribbean family and now, like oilseed rape, both these commodities have “neonic” pesticide issues constraining increases in home production;

our “low level” of sufficiency in potatoes, in part, is explained by the inexorable consumer shift to processed potato products (particularly French fries). Our import source are two small neighbours The Netherlands and Belgium who account for half the 10 million tonnes of processed potatoes exported globally. Why we’re not with them and could we be partnering global exporters as they run out of land at home for spuds are pertinent questions;

UK produced pig meat is at similar modest levels as potatoes. Most pork in the UK is consumed in processed form – retail sales of sausages and bacon are 3 times that of fresh pork. In history, Denmark dominated our bacon market and, from the very early 1900s we were reminded in their advertisements that “Good bacon has DANISH written all over it”!;

our lowest self-sufficiency is for vegetables and particularly fruit. The EU is the principal source for veg. and we scour the world for fresh fruit. Arguably, global warming may advantage domestic production of fruit, although traditional favourites apples & pears have struggled to compete with more fashionable fruit in our own domestic market;

cereal self-sufficiency has drifted lower since the hay days of EU membership but, at 79%, is well above the levels of the pre-1970s when Canadian wheat was principally used to make our bread. “Climate events” at home and abroad and global trade turmoil have brought increasing instability in domestic yields (and, thus, returns) and global supply.

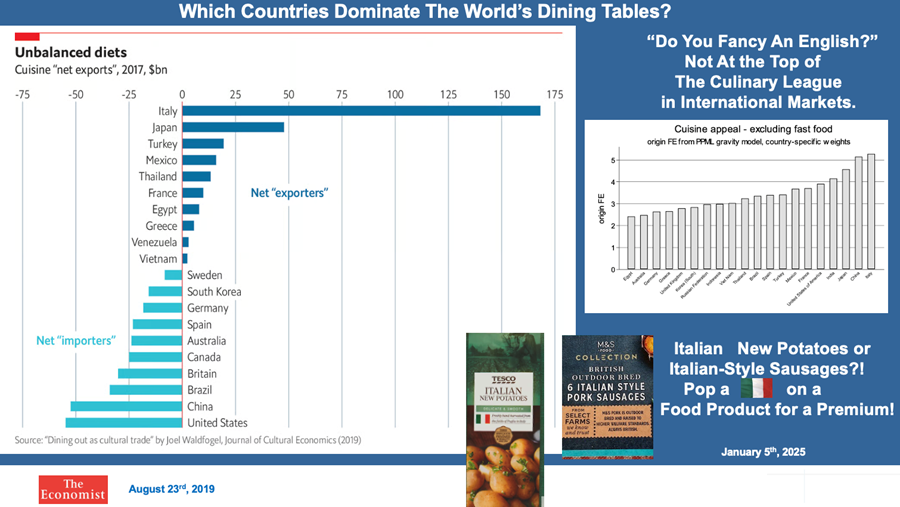

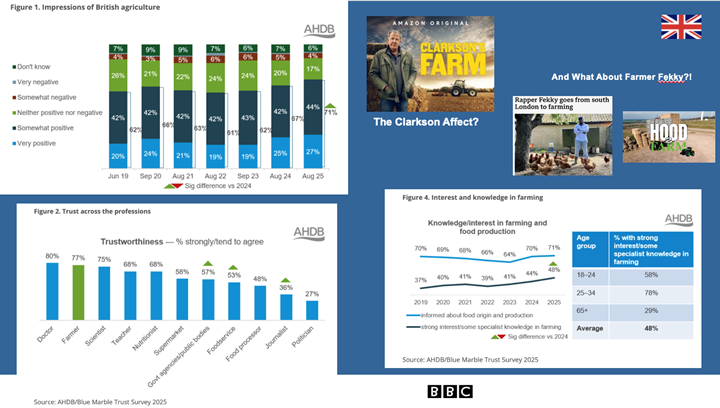

Returning to the mission “to grow the British brand for food & drink”, let’s start in our best market, i.e. The UK. Our consumers have a positive impression of British agriculture and accord farmers with a high level of trust. Interest in farming and food production is increasing, particularly amongst younger consumers (a Clarkson affect?). However, whilst they’re positive about British food, they also like imported foods. Why shouldn’t they as it’s been in our market for centuries. Preference for “my own country’s food” is highest in Italy – arguably, the country with the strongest food culture in The World. Italian cuisine, too, has pride of place on the dining tables of countries across the world, ahead of Chinese, Japanese and Indian meals. Tourists traversing the globe are unlikely to ask “anybody fancy an English?” when deciding what meal to eat of an evening! In UK supermarkets, food retail and food service is converging – shoppers are more likely to buy a meal than a collection of ingredients – and the meal can be selected from a panoply of international cuisines. The retail ready meals market, at £5.3bn. in 2025, was substantially larger than the combined retail sale of chilled beef, pork and lamb cuts. On ready meals, the UK is no global outlier. Buying the cooked meal from a market is common in Asia (e.g. Thailand) but there the meal is very likely to be traditional, local fare. Within our own market, a mention of Italy or France in relation to food, often as not, is associated with a premium priced product.

Buying a ready-to-eat snack/mini meal or full meal rather than the ingredients to make them presents a further challenge for our farmers as it places them one step back from the consumer by placing a food processor in between. If it’s a special snack/meal we may take the time to investigate the food story and explore provenance but if the meal is on the run, then, convenience of purchase and immediate consumption are the key drivers. Do you know anybody who has asked the doner kebab vendor “is the chicken free range?”! The consumer’s definition of convenience has been in flux for generations. For Gen. Z (30 years and under), convenient means NOW!

Across the globe, there’s a distinct trend towards international cuisines, in pure or hybrid/commingled form, particularly demanded by younger consumers (under-45s – Gen. Z & Millennials). Knowledge of and interest in “foreign foods” has been accelerated by social media. The rise of Korean food in the UK is a case in point – Korean pop culture spawned interest in other things Korean, including its iconic gut-healthy kimchi! Instagram and TikTok have been hugely influential in accelerating international food trends, with a quintessential example being the Canadian TikToker who, in 2024, generated a veritable tsunami of interest in Asian cucumber salads, and in the UK, 3 years earlier, Little Moon’s Japanese-inspired mochi (r)ice cream balls rocketed their way to retail success via TikTok.

What of the UK food consumer in 2026? British consumers have the lowest retail food prices in Western Europe (the UK grocery sector is the most competitive in the known world) but living costs are amongst the highest (bar Denmark and Ireland). Half of our households are struggling financially and seek to fill family tummies tastily but cheaply. Of course, family health is important and supporting home food producers but “needs must” and cost per calorie prevail making it challenging to pay a premium for local high standard environmental and animal welfare food.

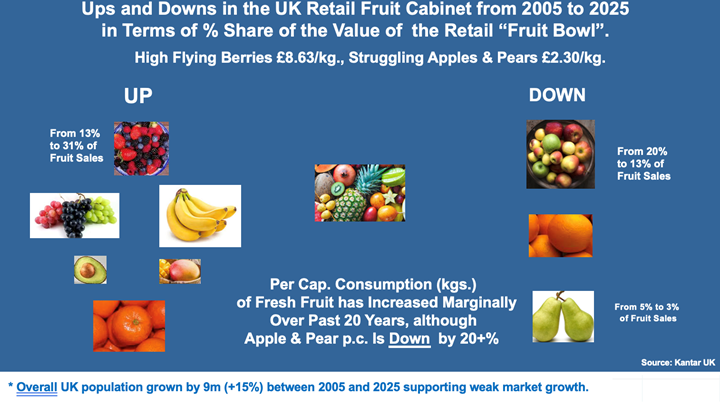

So, when shoppers are in the supermarket is it only about low price? Look at the ups and downs in the UK retail fresh fruit cabinet over the past 20 years. Keep in mind that for fresh fruit UK self-sufficiency (15%) is the lowest of any food category:

per capita fresh fruit consumption has increased over the 20-year period but only marginally.

the highflying fruit include imported easy peeler citrus, grapes, bananas, avocados, tropical fruits and fresh berries from home and abroad. The strugglers include oranges and traditional favourites apples & pears;

relatively high-priced berries (av. £8.63/kg.) have zoomed ahead of apples & pears (£2.30/kg.) jumping from 13% to 31% of retail fruit sales, whereas apples have declined from 20% to 13% and pears 5% to 3%. Clearly, in the mind’s eye of the shopper when choosing fruit, price is not the be all and end all!

Average weekly spend per UK household on fresh fruit is £12. Routinely, many city workers spend double or more than that on buying cups of coffee. Yet, in market research surveys, a common response when rationalising their modest fruit and veg. purchases is “I’d buy more but they’re a bit expensive”! If we want British shoppers to buy more home-produced food, then, we’ll have to up our efforts to communicate that it’s better value for money than the competition. Think back to the classic 1971 L’Oréal Paris beauty product strapline “because I’m Worth It!”. Amended, it works well for British food & drink: “Because We’re Worth It!”, the We being the consumer and family, the producer, society and the environment. We need to “de-commoditise” the British offer relative to imports. Tell the story and add adjectives because they add margin to all in the supply chain. Concomitantly, there’s a requirement that regulations ensure that imported food products match the standards required of domestic producers. Otherwise, the locals are on a hiding to nothing!

Expanding our food export opportunities will be principally focussed on premium overseas markets and the closer the better – 62% of current food exports go to the EU and 76% of our food imports come from there. They know us and we know them! The importance of introducing the proposed SPS (Sanitary and Phyto-Sanitary) Agreement to reduce import/export costs is commonsensical. Outside of the EU, particularly for premium cheese, the USA and high-income segments of Asian markets have exciting potential. But we won’t be swashbuckling our way across international food commodity markets, however, as we’re not low-cost producers relative to the agribusiness behemoths such as Brasil and USA. Further, like many industries, the agribusiness and food business world is polarising – the big are getting bigger. For instance:

in the Top 10 of world packaged food companies, 4 are meat producers (2 from Brasil);

JBS, the world’s largest food company, is extending its protein reach from meat and fish into eggs buying the largest egg company in South America and acquiring a Top 10 USA-based egg company. There must be something in the water in Brasil, fellow Brazilian Global Eggs is on a buying spree in Europe and USA, too;

the Top 10 global dairy companies each have revenues well above $10bn. and are hot foot to mop up smaller fry. Greedy? Maybe but you need annual sales above $500m. to capture scale economies;

horticulture has seen extraordinary global growth of big players – Driscoll’s in fresh berries, US-based Taylor Farms acquiring salad businesses in Europe, Shropshire’s and partners expanding;

Norwegian-based Mowi is the UK’s largest salmon exporter and, in addition to Scotland, is farming salmon in Norway, Ireland, Canada and Chile to give it a 20% global market share.

The stark reality is that the investment cost to continue at the leading edge of commercial food production is accelerating through this decade which is driving farm business consolidation (it’s been a trend for donkey’s years). Larger-scale agribusinesses and processors seek larger-scale primary suppliers. Small farm businesses can be efficient but, invariably, they require scale to be profitable. In history, UK farmers have shown reticence in collaborating to gain scale with farm partners. Smaller producers need to be “under the wing” of a larger business to gain access to volume markets unless they have the skills and experience to develop local niche markets. DEFRA analysis indicates that “the average farm all too frequently loses money on its agricultural activities”. Most farms gain income from diversification activities such as letting buildings, solar energy, tourism. In history, the Basic Payment Scheme subsidy was financially key whereas now, there’s reliance on less predictable “green operations” payments. Looking through the remainder of this decade, the pragmatist should place more weight on private diversification income than on public environmental payments. Domestic food production, care of nature, the ecosystem, and the rural environment are vital, but they won’t have the political clout associated with national health and defence spending.

The Cup of Coffee Version

Global food prices may have eased slightly, but they remain far higher than pre‑Covid levels, squeezing consumers while farmers face rising input costs, volatile trade conditions and extreme climate events. Food security has climbed the political agenda, fuelled by concern over reliance on a narrow group of exporting countries for key commodities such as coffee, cocoa, sugar and oils.

UK food self‑sufficiency currently sits at around 60%. Historically it has fluctuated: below 50% pre‑WW2, peaking above 75% in the 1980s, before drifting down again. Improving farming profitability and food security is now firmly back in focus. One route, recommended by Minette Batters in her “Farming Profitability Review” (December 2025) is to “grow, make and sell more from our farms by strengthening the British food and drink brand at home and abroad”.

Different commodities tell different stories. The UK excels at growing grass, yet has not become a major exporter of dairy or red meat, despite strong domestic production. Poultry is a success story, though imports are ever present in processed formats such as nuggets and kebabs. Sugar and oilseed rape face pesticide constraints. Potatoes and pork are largely consumed in processed forms, with neighbouring countries’ products strongly placed in our market. Cereals remain relatively strong, though yields and returns are increasingly volatile. Fruit and vegetables remain the weakest area of self‑sufficiency, but perhaps with advantages in prospect from climate change.

At home, British consumers trust farmers and feel positively about UK agriculture, particularly younger generations. However, they also enjoy imported food and international cuisines, which now dominate ready meals and food service. The UK ready‑meals market is larger than total retail sales of fresh red meat cuts, reflecting a long‑term shift from ingredients to prepared foods.

Convenience has become paramount, especially for Gen Z, where “convenient” means immediate. As processors increasingly sit between farmer and consumer, provenance often fades from view unless the product is positioned as special or premium. International cuisine trends, amplified by social media, continue to shape demand. Korean food, Japanese‑inspired snacks and viral trends illustrate how quickly tastes can change. These forces are global and unlikely to reverse.

British consumers benefit from some of the lowest food prices in Western Europe, yet living costs are high and half of households are financially stretched. Price matters, but it is not the only driver. Fruit purchasing patterns show that consumers will pay more for perceived value, as seen in the rapid growth of berries despite higher prices.

If domestic production is to grow, British food must be “de‑commoditised”. Storytelling, provenance and standards matter. For more special meals, consumers seek food with adjectives that have redolence! Communicating value — not just price — is essential, alongside ensuring imported foods meet equivalent standards so domestic producers compete on fair terms.

Export growth will focus on premium markets, particularly the EU, which remains our closest and most important trading partner. Beyond Europe, opportunities exist in the USA and high‑income Asian markets, especially for products such as cheese. However, the UK will not compete on low‑cost bulk commodities against global giants.

The global food industry is consolidating rapidly. Large agribusinesses and processors increasingly dominate, driving scale requirements throughout supply chains. Investment costs continue to rise, pushing farm consolidation. Smaller farms can be efficient but often need collaboration, niche markets or alignment with larger players to remain profitable. Public support is becoming less predictable, and diversification income is increasingly important. While food production and environmental stewardship are vital, long‑term resilience will depend on commercial viability. Expanding UK food production is possible, but it will require realism, scale, collaboration and a stronger value proposition for British food — at home and abroad.

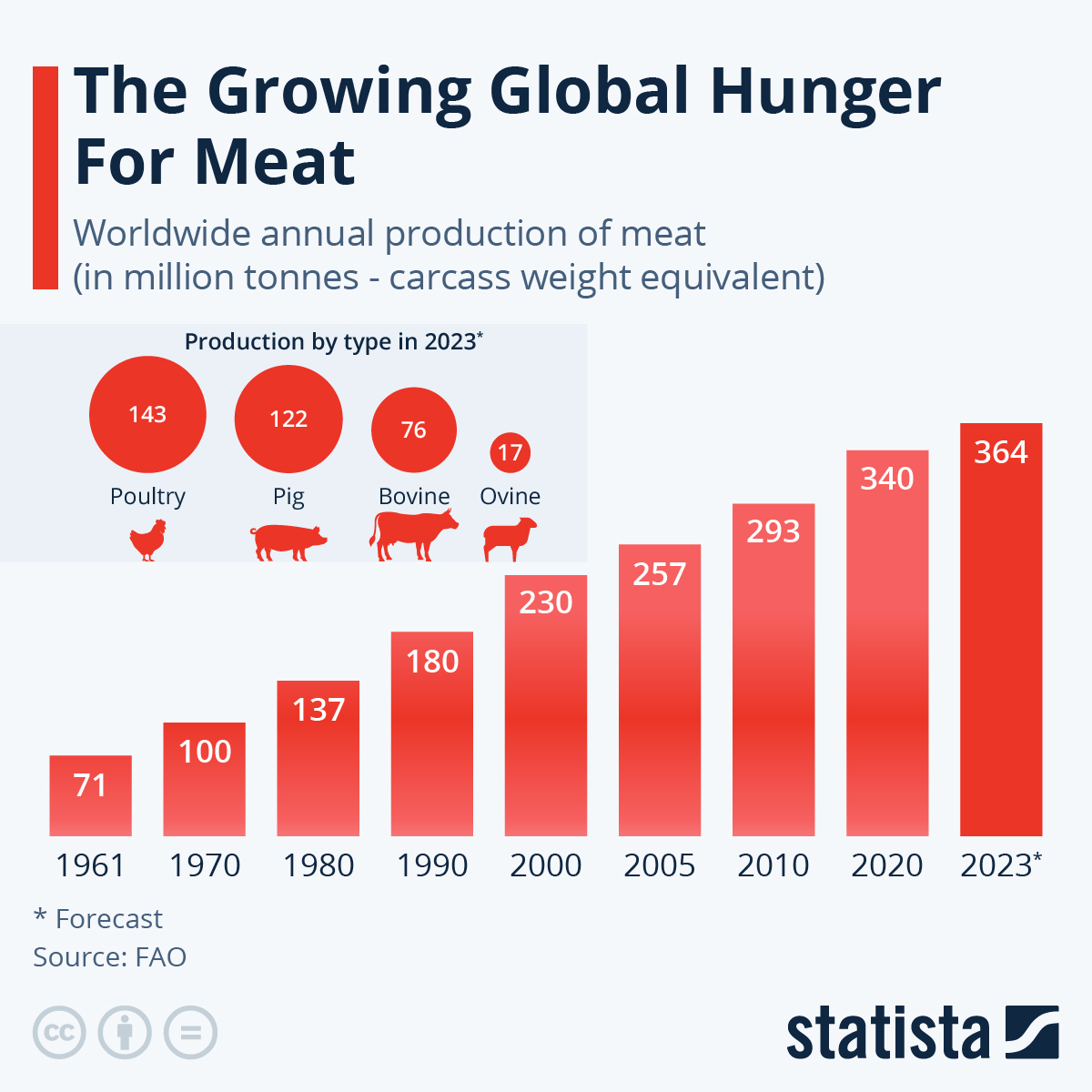

Who’s top of the global league in land-based meat consumption? It’s chicken, but that wasn’t the case 12 years ago. Whereas ALL the major meats (chicken, pork, beef, lamb) have seen global market growth since 2013, chicken has screamed ahead tipping pork from the top position: in 2025, chicken has a 41% global meat market share (up from 36% in 2013), pork has a 34% share (down from 38%), lamb holds steady at 5% through this period, and beef has slipped from 22% to 20% global share (Gira estimates). Over this12 year period, our world population has increased by 1 billion and is responsible for driving the 20% total increase in meat volume sales. However, if your measure is meat consumption per capita, chicken rose by 23%, minor meat lamb saw some growth, whereas pork and beef drifted lower.

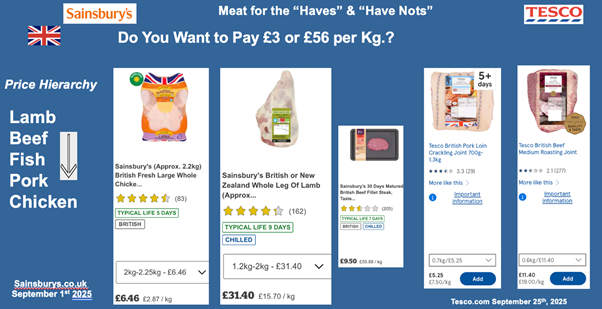

Likely, the position of red meat, struggling since the pandemic through a prolonged “cost-of-living crisis”, from a consumer perspective, will continue to see thin times in terms of growth. Browse the UK supermarket shelves for your Sunday roast: chicken is astonishingly affordable at less than £3/kg.; pork at £7.50/kg.; leg of lamb at £16/kg.; and beef at £19/kg. – a clear indication that there are meats for the “Income Haves” and for the “Income Have Nots”. The latter, often, 40% or more of all households perceive they have little option than to seek high calorie-low price meal options for their families – a 30 pack of breaded chicken nuggets, plus 1.5kg. of frozen French fries, and, say, 2 “snacking” small pizzas costs £4.65 ($6.26) to feed a family of 4 or 5 from Tesco (and these items are all Aldi price-matched). That amount will barely buy you a couple of lamb chops!

Consumers are not doomed to a low-income growth future and, in many countries, when the tide turns, meat consumption will tick up. People in richer countries tend to eat more meat and, certainly, more premium meats. There are outliers where incomes are relatively low but beef consumption is high – BBQ-loving Brazil with its churrascos and Argentina with asados come to mind. Mind you, high income countries don’t necessarily see sustained growth in meat consumption and the UK is a case in point. Our per capita meat consumption has drifted down over the past 20 years, BUT overall meat market volumes have grown as our total population has increased by 10 million over this period. Like most European countries, Australia & New Zealand, USA and Canada, population growth has been driven by incomers and reminds one that it’s handy to keep a tab on the meat preferences of the newer arrivals.

So, in the UK are we going off meat? Far from it! We’re eating less meat per person but we’re not eating meat less times. Our meals, even savoury snacks, may be meat-based but there’s less meat in meat portions, ready meals, sausage rolls/pasties, etc. and we are an ageing country. Old folk eat less. UK median age is 41 but that makes us youngsters relative to Germans (46), Italians (48) and the ancient Japanese (50)! And look, with some country exceptions (e.g. Bangladesh), the world loves meat and are VERY reluctant to give it up notwithstanding exhortations about the impact of animal production on the environment and on our health if we are meaty over-indulgers. Meat consumption is in our genes. As the brilliant cartoon showing stick like stone-age figures hunting game advises “We have never found a cave painting of a salad”!

In the USA, poultry (specifically, chicken) is King of The Coop. Overall meat consumption continues its slow but seemingly inexorable upward movement and reminds one that, in America, if something is worth doing, it’s worth doing to excess! Of the 100+kg. per capita of meat consumed each year, poultry accounts for 51% of total, up from 25% back 50 years ago, beef’s share has dropped from 45% to 26%. Per capita pork consumption was above chicken in 1970 at around 25kg. and it remains at this level to this day, whereas per capita beef consumption has declined by 33%. Lamb is essentially a specialty meat in the USA and the cayotes eat more domestically produced lamb than do its citizens!

Addressing the market position of chicken, why is it so successful? Straight off, it’s relative low price and, through time, the relative ease of deconstructing the carcase with machinery not labour. But, back to the USA again. In 1970, per capita chicken consumption was 22kg. (18kg. in UK) and by 2024, it was at a meaty 53kg. (35kg. in UK). In the 1950s in most British families, chicken was for Christmas, now, it’s “Chicken Tonight”! Chicken has been consistently closer to the consumer and to emerging trends than the red meats. McDonald’s NPD and promotional oomph has been helpful – in the USA, it launched “Southern Style Chicken Biscuits” for breakfast in 2008 and pushed the chicken breakfast boat out comprehensively nationwide with Chicken McGriddles in 2020. The relaunch of the McDonald’s Snack Wrap in July 2025, gained international headlines in the popular press. If you can add another eating occasion (e.g. breakfast, mid-morning snack), then, whoop-de-doo!

As diets around the world have become more international (e.g. Indian, Mexican, Chinese, Thai), the focus has been more on the sauce than on the meat species and, because of its price, chicken has become the default meat option. Additionally, chicken meals are seen, often, as being more versatile and family-friendly than other meats (kids like chicken, well nuggets) and have no religious barriers. As life has picked up speed, we’ve changed the way we eat and drink. More recently, traditional meal patterns (“3 meals a day”) have fallen away and now, mini meals and snacks are increasingly prevalent. As Kantar aptly puts it, “what was once called “convenience” has become something more – flexibile (and, a vital companion, affordable). It’s more than grabbing something on the go or just being super quick, it’s about finding food and drink that can bend, twist and fold itself into the unpredictability of modern life”. That’s chicken!

Keep your eyes on Generation Z (i.e. consumers who are in the age range 13 to 30). They’re 4 times more likely to select “grab & go” meals/snacks than ageing boomers. How do they define convenience? Succinctly, now means NOW. Processed chicken products are the default choice and air-frying the means of final meal preparation. Increasing protein intake is fashionable for those in their late teens and early twenties. Again, chicken fits the bill. In the UK, the range of The Gym Kitchen products hits the mark. In the USA, Tyson offer NFL Kansas Chiefs nuggets. What about Liverpool FC “Reds” chicken bites? Keep in mind, meat isn’t the only protein source, and the market is getting crowded, not least with dairy products and nuts.

Captain Birdseye’s seafaring days may be limited. He’s heading for the shores and the chicken shed – note BirdsEye chicken (not fish) fingers, and chicken (not potato) fries. Perdue “Sea Creature chicken nuggets” has enough cheek for another row of teeth with its “fun shapes of fish/turtles/shrimp/octopus” made from chicken.

Meat sticks are becoming America’s favourite new snack, and we’ve moved on without displacing biltong. There’s room for all meats to do well here but, in the UK, chicken snacks are leading the charge. There’re even crisps (chips in the USA) made from chicken breast and chicken crackling (fried chicken skin) sitting aside the traditional favourite pork scratchings.

Remember that close to 40% of UK households have a family member that isn’t human – the dog, that is, not the difficult partner or child. Mabel, the “Sprocker” in David’s home, demolishes 1kg./week of Tesco’s chicken thighs giving her a per capita consumption 50% above average for our nation! Spoilt rotten? Undoubtably, but at £3/kg. courtesy of the low fresh chicken price, it’s the same cost as a can of Butcher’s Tripe dog food!

Will chicken retain its paramount position amongst meats? Browse the meat aisles in our supermarkets. Chicken gets 3 times the shelf space of beef and 5 times that of lamb (for goodness’ sake, in Waitrose, Charlie Bigham’s posh ready meals get double the space of lamb). Pork holds its own courtesy of serried shelves of bacon and sausages. But, move over an aisle and you’re into stacks of prepared meals, easy meals, the “that’s dinner sorted” and snacking & sharing sections. In these areas, chicken has a disproportionate share of the protein on offer. In short, we’re nowhere near “Peak Chicken”. Pork, in its processed form, has opportunities here to build on its traditional base of cured meats and expand its snacking offer.

As food retailing and food service converge, which is happening at pace particularly in the UK, meat isn’t sold as meat cuts, per se, but as the meal and/or snack solution. As those Gen. Z consumers grow older, they’ll require a shopping assistant to show them where and how to buy raw meat. For them, it will be an exciting outing enjoyed once or twice a year, like going to the zoo!

For domestic producers of meat (i.e. farmers producing livestock for their national market), a worrisome implication of the trend towards consumers eating meat more in processed form than fresh is that it increases the opportunity for lower cost international meat producers to broach new markets – for example, if pork or chicken are the ingredients in a “value-added” processed meat product rather than the product itself, as they would be if on the chilled meat aisles of a supermarket, the less notice consumers will take of the origin of the meat ingredients. This risk is similar for meat sold via value/cheaper food service outlets – most consumers don’t ask “where does this chicken come from?” when buying fried chicken or nuggets at the end of a boozy night out, or when tired children are screaming for food towards the end of the afternoon of a family outing!

To finish, seafood competes directly with land-based meats for the household protein and “Centre of the Plate”. Rabobank advise that “seafood is poised to surpass poultry as the leading contributor to global protein supply growth”. Sea creatures are the Number 1 meat in Portugal. In many Asian countries, seafood consumption is at or above “chicken levels”. Some fish species can compete on price with chicken – Pangasius, a pond fish, aka catfish or Basa. It’s a tasty fish for the “Income Have Nots”, whereas “Income Haves” can feast on wild salmon, tuna and lobster, with middle incomers selecting farmed seafood such as salmon, sea bass and prawns. If you’re in the meat business, then, you’re into protein whether it’s produced on land or in the water.

Keep in mind that the world’s biggest packaged food company and, certainly, the largest protein company is the Brazilian behemoth JBS (food revenues of close to $80bn. in 2024). JBS started in beef, added pork, chicken and lamb, moved into farmed salmon and has just acquired a company to make it the largest egg producer in South America. Its intent? To consolidate and enhance its position as the world leader in protein for human consumption. There must be something in the water in Brazil! Its biggest competitor Brazilian company Marfrig (the world’s 7th biggest packaged food company) has just gained approval to merge with BRF (Brasil Foods) to increase its international competitiveness. Four of the ten largest food companies in the world are in the meat business. The big are getting bigger presenting challenges to those “stuck in between” as to where and how they can differentiate their products and services and best ply their trade.

Wherever one looks. North America, Europe, Australasia, Japan, per capita fresh fruit and vegetable consumption is drifting downwards. What’s going on? Everybody knows that they’re essential for our health but very few of us get even close to meeting our 5-a-day targets. The UK Eatwell Guide and the New Zealand equivalent infographic are resplendent with fresh produce which look pretty on the kitchen wall, but they attract dust rather than attention! Fresh produce market volumes may show a slight increase, but these are driven by rising population not individual households eating more.

The most influential factor constraining growth in many countries is the rising retail prices of fresh fruit and vegetables. Recent Reserve Bank of New Zealand research notes price increases of 45% between 2014 and 2023 outstripping those for processed foods which rose by only 14%. For those households challenged to pay their mortgage/rent, grocery bills, energy and transport costs, etc., and such numbers have mushroomed during the 2020s, filling family member tummies has become a price per calorie battle and processed foods, typically HFSS (high fat, sugar, salt), are a fraction of the cost per calorie of most fresh fruit and vegetables. The UK Food Foundation calculates that “value” ready meals and processed meat are half the calorie cost of fresh fruit & veg. Dismally, escalating fresh produce retail prices are not necessarily reflected in higher prices to farmers. Their production costs have risen disproportionately, and their margins squeezed by ferociously competing retailers. What hasn’t helped has been extreme weather in many parts of the world causing supply chain disruptions driving prices even higher. Processed food companies have been more adept at capturing the eye of the food consumer through tracking and responding to consumer trends and launching promotional initiatives whereas fresh suppliers, typically, have focused on producing and relying on their retail customers to present and promote produce as they seem fit!

So, when it comes down to selecting our food products, is it only about price? Not necessarily. Take the UK fresh fruit market where the outstanding category over the past 20 years has been fresh berries. This year, fresh berry retail sales are 30% of the total retail value of all fresh fruit. 10 years ago, that figure was 20%. Yet, fresh berries have an average retail price/kg. 4 times that of apples which have seen their value market share of the UK fruit bowl slip from 21% to14% over the same period. Clearly, shoppers will pay more for what their families enjoy even although it may pinch their purse. The success of fresh berries has been global: taste and 52-week availability have been transformed; they’re snackable and firm family favourites. In the UK, casting back over the past few decades, snackable fruit such as berries, grapes, easy peel citrus have burgeoned whereas traditional favourites such as apples, pears and oranges have floundered. Mind you, the world’s most consumed fruit, bananas, combines snackability, strong kids’ acceptance and low price – feel sorry for Latin American producers because, in the UK, retail prices for bananas are the same as they were 20 years ago. At less than £1/kg. bananas are essentially a “free good”.

It’s a truism that fresh fruit and veg. are indispensably healthy but are perceived to be expensive. In consumer surveys across the globe, a common response is “I’d like to buy more but they’re kind of expensive”. Yet, many urban workers spend twice as much on their coffee purchases in the week than they do on fresh fruit & veg. for the entire family! Sadly, fresh produce is not addictive like coffee, nicotine and alcohol. The challenge is to present fruit & veg. in a form that meets consumer requirements and to communicate its cracking value for money and contribution to family health.

Whilst fresh fruit & veg. per capita consumption may be down in the dumps for some produce, but that’s not the case for frozen produce. In the UK, both frozen fruit and vegetables have seen modest but consistent upward movement over the past decade, accelerating through and after the Covid period as households saw advantages of frozen in terms of price, storability (shelf life) and reduction in food waste. Focussing on vegetables, it’s probable that this trend may be longer-term. Clarence Birdseye gave them a start in 1929, not least with peas and, in the 1940s, the Simplot Company caused a splash with frozen French fries. Who shells peas from fresh now or peels and slices potatoes to fry on the stove for chips? Cadbury’s iconic Smash Martians popularised “instant” mash potatoes in the 1970s (remember the advert.? “For Mash Get Smash”) and the brand is still on the UK market courtesy of Premier Foods even now. However, chilled mash potatoes for long a popular item in the USA (Kroger supermarket chain has 386 chilled mash products on its website) are now having a day in the UK and elsewhere. Tesco has 20+ mashed potato products online and the standard own label mash at £1.32/kg. (US$1.77) with a Clubcard is a snip.

Consumers aren’t quick to embrace new forms of traditional products, but they do move along a continuum, taking chilled mashed as an example, from Never to Occasional to Routine purchase through time. Convenience is an overwhelming driver! It’s a route that is likely for vegetables that are most under the gun in terms of family acceptance – such as “the hard veg.” beetroot, carrot, parsnips, squash, sweet potatoes sliced, frozen and ready for air frying. Chilled, chopped onions are another value-added product that is edging its way into the fridge of would-be meal preparers who are short of time.

What of frozen fruit and ambient processed fruit products. They don’t count in our measure of fresh fruit, but they are pervasive and growing in demand. We train our children to consume fruit from pouches. They progress through childhood into early adulthood swigging fruit smoothies. Per capita fresh pear consumption is dwindling in the UK. Indeed, every time David sees a hearse go by, he’s anxious on 2 counts: could it be one of his mates; and, for certain, there goes another pear consumer given the ageing demographic of the UK fresh pear market! The baby that sucks from a pear pouch will progress to slurping a fruit smoothie snack (1 of your 5-a-day) and on to the giddy heights of a super smoothie as their fruit palette sophistication blossoms to enjoy squished lychees, apples and dragon fruit with extra vitamins. Frankly, if you gave most UK teenagers and early-twenties a fresh whole pear, they wouldn’t know what to do with it!

Returning to the giant pumpkin in the room, i.e. declining per capita fresh fruit & veg. consumption. Does it matter? Well, yes if you believe that fresh fruit & veg. have a contribution to improving the dietary health of the world. Notwithstanding the emerging prospect that AOMs (Anti Obesity Medications) are arriving, like the cavalry, to stem the global obesity crisis. Worldwide, governments are desperate to encourage healthier eating. The UK has released a 10-year plan for our creaking National Health Service and has an agreement with major food retailers and manufacturers for them to report, using an accepted nutrient profiling model (NPM), progress in increasing the proportion of healthier (i.e. non-HFSS) foods and achieving stretch targets. This sounds positive for those in the fresh fruit & veg. business! Our major supermarkets are in concert with the aims: Tesco will reward customers with extra Clubcard points for buying more fresh produce; Sainsbury’s has a somewhat more complex programme, based on its Nectar loyalty card, for those buying “Healthy Choice” food products. Others across Europe are on the same page. Even the normally disciplined, super fit, stick thin Swedes (the nation not the vegetable) – ICA the grocery market leader in Sweden is lowering prices for key fruit and veg. items and launching “Join the Fruit Reboot” presenting fruit in a more modern, child-friendly way (only 1 out of 10 Swedish children achieve their 5-a-day target). In the UK, VegPower has seen success in casting vegetables as villains and calling on children to “Eat Them to Defeat them”. In Australia, the International Fresh Produce Association (IFPA) has launched its “Fruit and Veggies Yummy Yummy” campaign with The Wiggles Family encouraging children to explore, cook and enjoy fresh produce. All of these initiatives are helpful but far from being sufficient.

To revisit the 2 principal reasons why per capita fresh fruit & vegetable consumption is declining. First, exacerbated by many households being in “a cost-of-living crisis”, there’s the high cost per calorie of fruit & veg. and, even when through retail promotions fruit & veg. can be astonishingly (from a producer perspective, worrisomely) affordable, it’s perceived to be “kind of expensive”. Yet, in the UK, average weekly household spend on fresh fruit & veg. is only £12 (US$16). Second, even although most shoppers intrinsically know that serving more fresh fruit and veg. is in the best health interests of themselves and family, if the kids don’t like it and if it takes time, and for some, knowledge to prepare it, then, we’ll skip it and buy something pre-prepared. These are tough negatives but, onwards! We must accept that convenience invariably trumps health concerns. How a Baby Boomer (60+ yrs.) defines convenience bears no relationship to how a Gen. Z (13-28 yrs.) defines the term. Going forward, fresh fruit & veg. will increasingly be sold in a “value-added” format – removing labour and need for expertise from its preparation and use in meal/snack-making. Remember, whereas David’s Mum used to pop down to the grocer to buy ingredients, Gen. Z are not even familiar with the term and simply seek meal and snack solutions.

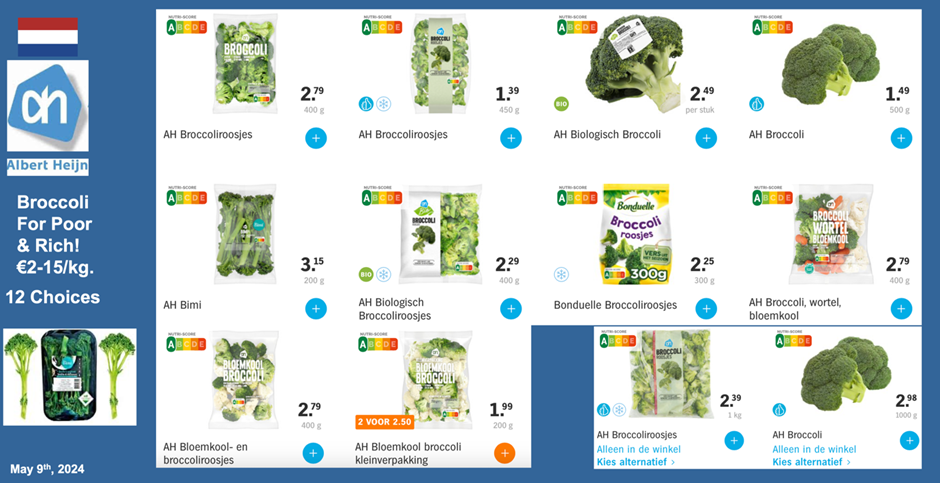

Retail presentation can be much improved for fresh produce, often, by simple cross-merchandising. For, say broccoli florets, make sure they’re adjacent to appropriate dips, sauces, hummus, etc. Marks & Spencer place the cream next to the strawberries. Avocados are in vogue and place the whole fruit next to the guacamole and avocado smoothies. For any fruit and vegetable item, take a leaf out of the avocado marketing book and create/magic up another eating occasion for your product – smashed avocado as a breakfast emerged in Australia in the 1990s and quickly became fashionable around the world. Is there a TikTok marketing opportunity for you? – check out the Canadian TikTok cucumber salad champion who rocked the global cucumber supply world!

To finish, fresh fruit and vegetables are widely considered the quintessentially healthiest food category. Yet, consumers elect frequently to ignore this attribute in our choice of food. We observe that within the fresh produce departments of most supermarkets, there is VERY little noise made about the specific health attributes of produce. If you want to know about how healthy berries and cucumbers are, go to Boots the Pharmacy and browse the beauty product shelves!

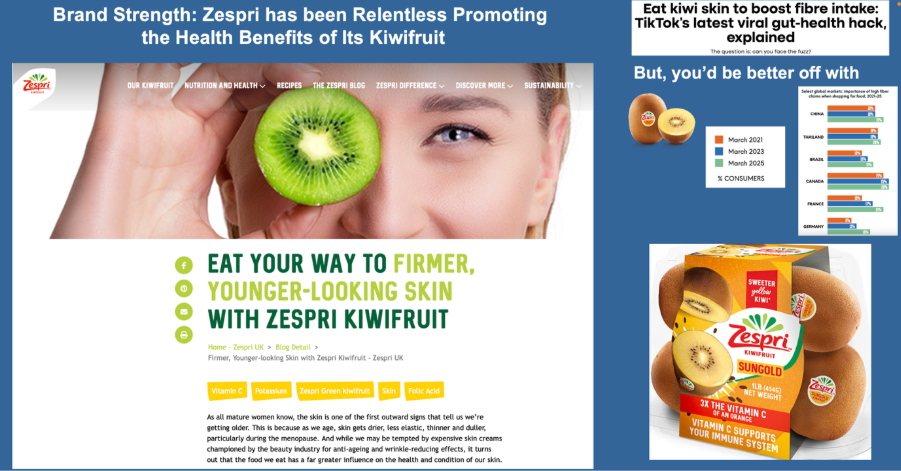

Some internationally branded fresh produce companies do promote their products on health – Zespri comes to mind (their kiwifruit vitamin C content being double that of oranges!). In China, Joyvio. the blueberry brand leader identifies eye health as the key attribute. Why is the fresh produce industry so shy in front of the shopper? Is it because we have a commodity orientation and who’s going to pay for the promotion? Scottish premium salmon trumpets that 1 salmon fillet provides our omega 3 requirements for the week. It’s important to identify the specific health benefits that attracts each consumer group – such as heart health for the older, skin health particularly for women, brain health for Mums (not theirs, their children!). At a time when consumer concerns about UPFs are on the rise, make sure that on your front of pack you have your ingredient list, e.g. for carrots, state Ingredients: Carrots!

If you’re still with us, Thanks. Do enjoy your Summer in the Northern Hemisphere and wear wool next to your skin in the furthest southern part of the Southern Hemisphere.

If you’re in the fresh produce business, you’d think it reasonable to conclude: “right time, right place”! Around the globe, consumers put “eating more healthily” pretty much at the top of their “To Do” list for 2025 and it’s for good reason as, increasingly, the majority of the population are as round as puddings. Prestigious medical journal The Lancet forecasts that more than half of adults and one-third of children worldwide will be overweight or obese by 2050. Yet, eating healthier is easy to say and, clearly, difficult to do. Eating more fresh fruit & veg. would be a good start. And that’s exactly what people aren’t doing! What’s the story?

Take higher income countries, across the EU, UK, USA, New Zealand and Australia, longer term per capita fresh produce consumption has trended downwards – although market volumes may have increased driven by increases in population. Economic downturns are not a friend of the fresh produce industry and the current “cost-of-living crisis” is a case in point. In regular times, fruit and vegetable consumption by lower income urban families is significantly less than in better off families. When the purse is pinched, this is simply accentuated. Through the past few decades, cost per calorie of “value”, albeit unhealthy foods, such as some cookies, cream cakes, skimpily covered pizzas have become substantially lower than healthy foods such as fruit & veg. and they provide convenient, low-cost meal solutions and assuage hunger whereas salads, cabbage and apples don’t! Most Western countries are far from achieving anywhere near their 5-a-Day F&V targets (exceptions being Greece, Belgium, Italy, Portugal, and Poland) and there’s been a pervasive drift, across most continents, towards an American-style diet, i.e. one characterised by a high proportion of the controversially defined Ultra Processed Foods (UPF). By the bye, females are more fresh produce friendly than males, particularly if they have small children (and the urban myth is that a Glaswegian male is more likely to be seen doing needlepoint than eating fresh fruit!).

The market is flooded with convenient solutions to fix a meal in no time.

So, do we just need to lower prices to increase consumption of nutritious fresh fruit & veg.? No and, fresh produce growers, park your anger for the moment at the thought of doing such! Here’s a mini case study on the UK fruit market. Keep in mind that this market is largely serviced by imports – 56% from outside Europe, 28% EU, and a modest 16% home-produced. Over the past 15 years, per capita fresh fruit consumption has seen a tiny increase (3%) and is about 40kg/cap. From 2010 to 2024:

Total fresh fruit retail market value increased from £4.1bn to £7.2bn and volume from 2.47m to 2.8m tonnes while UK population increased from 62.8m to 69.1m;

In volume terms, bananas continue to be the UK’s favourite fruit, followed by apples, and citrus but all three have slipped in the consumer’s affection, whereas the composite category berries have close to doubled their share, tropical fruit have advanced significantly and grapes have edged forward. Pear volume share of the market has nigh on halved (with the worrisome thought that, given the demographic profile of a typical pear eater, every time one sees a hearse go by, there goes another pear consumer!);

Is price driving consumers’ choice of fruit category? Perhaps surprisingly, NO! Fresh berries have a retail price point/kg. some 4 times that of apples and pears, and 8 times of bananas, yet from 2010 to 2024, fresh berries have increased their value share of the retail fruit bowl from 17% to 29% of total and look on course to taking a full one-third of retail fresh fruit sales by decade end (with blueberries leading the charge). Bananas, at £0.99/kg, are essentially a “free good” and have seen less than a 10% increase in retail price over the 15-year period, whereas average retail apples prices rose 47% from £1.45 to 2.13/kg and berries by 48% from £5.71 to £8.47/kg. Do such increases compensate fruit growers for input cost increases? Far from it. For berries, labour costs account for around 50% of total costs and minimum wages have doubled from 2010 to 2025;

The UK is an intensely price competitive market with supermarket own label products dominating. The 2 principal hard discounters – Aldi and Lidl – have had huge success in expanding fruit value market share from 6% to 22% at the expense of traditional supermarkets and the dwindling independent trade ensuring inexorable downward pressure on retail F&V prices;

Low although prices may be, there’s positive news for the UK fruit industry in that retail fresh fruit market volumes peaked in the tragic home-incarcerated Covid years of 2020 and 2021, then declined in 2022 when we were “released” but recovered in 2024 to close at the previous peak levels;

Of course, consumers have other choices than just fresh F&V and, particularly for vegetables, in the UK the Covid period saw a boost in frozen purchases driven by its longer shelf life, perceived convenience, less waste than fresh, improvement in consumers’ perception of the nutritional quality of frozen produce, and the relative price competitiveness of supermarket branded frozen vegetables. Best keep an eye on which veg. will follow the lead of frozen peas and French fries. Chilled ready mashed potatoes are becoming a routine purchase for many households and, looking to the future, frozen chopped onions and garlic look likely candidates for sales growth. Constraints to the expansion of frozen include availability of freezer space in the home, and concerns about “additives” in frozen products.

Pineapple aroma and a hint of vanilla… it’s not your wine, it’s a pale strawberry!

Major factors underpinning the success of relatively pricey fresh berries in so many markets include: they’re perceived as a treat (and even in stringent economic times, who doesn’t need a treat?); loved by children; crucially, they’re convenient (you don’t have to peel them!) and intrinsically snackable; seen as health heroes, particularly blueberries; widely available year-around which encourages weekly “routine purchases”; emergence of berry brands and “good/better/best” tiers; and, like some other fruits, accelerated investment in R&D has delivered notable improvements in the qualities appreciated by customers (e.g. consistent delicious taste). Zespri’s Kiwi Gold and RubyRed kiwis are good examples of combining the power of intellectual property and branding to “decommodify” the more generic green kiwifruit category. All produce items need to avoid “the commodity trap” epitomised by bananas – with 99% of those internationally traded being the Cavendish variety. Famous brands are associated with the fruit – Dole, Chiquita, Del Monte, Bonita, Fyffes and more – but few, if any of these generate a significant brand premium (would you switch supermarket because they’re out of Dole bananas rather than your regular Chiquita ones?). Bananas have the dual function for the supplier of delivering huge volume in shipping such that they can inexpensively add on other higher margin produce.

Returning to the healthiness of fruit and vegetables, where can customers garner compelling claims as to the benefits of fruit and veggies – the fresh produce aisles of supermarkets? No – wander around pharmacies such as Boots and note that cucumbers and berry extracts are lauded for their skin beautification properties. In the premium juice and smoothie aisles of supermarkets, product labels are crammed with claims relating to F&V portion equivalents which can be ingested with a few glugs in seconds! Tesco.com is a case in point: there are hundreds of fruit and vegetable drinks, juices and smoothies on offer: e.g. happy monkey smoothies … and on front of pack “made for kids with 100% fruit, No Bits (God forbid!), no additives or added sugar, 1 full portion of fruit, great for lunch boxes”. Are these fresh fruit and veg. competitors? Sure, why bother buying the real thing? In the fresh produce industry, we’ve largely relied on others to make motherhood claims about our F&V. But, claims that they are “a good source of vitamins and minerals” are insufficiently visceral, they don’t connect. At a time when consumers say they want to eat more healthily, they seek specific credible information on what the benefits are to me and my family (and, more challengingly “how long before I can see the benefit?”). Joyvio, the leading fresh blueberry brand in China, hits this nail on the head – its claim that blueberries improve/are essential for eye health is widely embraced by consumers.

Across the globe in the fresh produce industry, rapid change is afoot. Commercial horticulture is simply increasing in scale. The investment cost to be at the leading edge of fruit & vegetable production is accelerating through this decade and will continue to do so. Mid-20th Century saw the global “Green Revolution” fuelled, in part, by significant public sector funding (e.g. World Bank) but, now, the “HortiTech Revolution” is dominantly private sector funded and there’s a substantial entry cost for those horticultural businesses wishing to be on board. You want to reduce in-field labour costs and cut out herbicides? The smaller “LaserWeeder” costs you US$600K and its big brother $1.5m. Harvesting robotics are still at an early stage but will be with us at decade end as will profitable, albeit eye-wateringly expensive, advanced vertical farming. Horticultural crop breeding is being transformed by a combination of AI and gene editing (e.g. look at what Heritable Agriculture and AddGene have to offer). Just as we are seeing polarisation of income in consumer markets, i.e. household income “haves” and a high proportion of “have nots”, there’s polarisation in horticultural businesses, for example: fashionable, high growth berry and avocado sectors are seeing massive consolidation (note the acquisition journeys of Driscoll’s and Westfalia Fruit); in Australia, 10 horticultural businesses, some infused with private equity investments, account for over 50% of fruit & vegetable sales; branded bag salad giant Taylor Farms in the USA is investing in the European salad sector; G’s Fresh in the UK with $1bn sales of salads, celery, beetroot, asparagus, onions and more identify wherever they can establish a Number 1 or 2 supplier position with UK supermarkets; in varietal development and licensing, Sun World International for fruit and Sakata for vegetables are expanding; and, of course in frozen potato products, McCain’s, Simplot, Lamb Weston and Aviko sit astride the rapidly expanding world of frozen French fries.

If the Big League horticultural players have, inter alia, economies of scale, financial capacity to harness technological innovation, ownership of/exclusive access to valuable varietal intellectual property (IP), a consumer relevant brand and a suite of major supermarket customers, where does this leave smaller-scale fruit & vegetable businesses? In short, they’re scrambling! Food producers across the world are grumpy but horticultural growers are a step above grumpy and into incandescent rage territory. For example, one-third of Australian vegetable growers are considering exiting the industry. It’ll be a similar figure for UK fruit growers who have only a small proportion share in their home market. Can growers strengthen their position? Options can include aligning their own businesses with those with IP and brands, for example:

the New Zealand Government-owned Institute for Plant & Food Research is adept at developing partnerships with grower-owned Zespri, the No. 1 global kiwifruit exporter, and with venture capital-owned Rockit exporting “mini-apples in a tube” to 20+ countries;

California-based Sun World was a pioneer in the fruit industry to work with select growers and marketers worldwide in introducing new varieties of grapes (e.g. Applause and Epic Crisp last year) and stone fruit;

Japanese seed company Sakata partners with marketing organisations in Europe (Bimi/Tenderstem), USA (Baby Broccoli), Australia (Broccolini) who work with local growers to produce the popular green vegetable which is a cross between Chinese Kale and broccoli and sells at a substantial price premium to commodity broccoli. Apple & Pear Industry Australia representing Australian apple and pear growers uses a similar approach to Sakata in marketing Pink Lady apples around the globe. Pink Lady are grown in Australia, New Zealand, Europe (but not yet in the UK), South America and South Africa and achieve a mouth-watering price premia in Europe and beyond;

G’s Fresh in the UK works with growers and cooperatives in the UK, Poland, the Czech Republic, Spain, and Senegal to supply salad crops and vegetables (largely supermarket customer branded but with some G’s brand such as LoveBeets) to major retailers in the UK;

Should small-scale horticultural businesses consider using their scarce resources in other ways? Why wouldn’t you if you were beating your head against a wall! But, smaller-scale can work in servicing very local markets with strong customer connections, and/or wider markets with more niche, specialty fresh and processed products. In the UK, the tiny Isle of Wight provides examples – The Isle of Wight Tomatoes with its fresh tomatoes and tomato condiments, and The Garlic Farm with fresh garlic, plus a host of processed garlic products and tourism. David has his own personal experience as co-owner of a small hydroponic herb farm in Florida which developed a range of branded packaged fresh products selling consistently at a premium to the commodity herb market. But, keep in mind, whilst Ernst Schumacher advised us that “Small is Beautiful”, in a mid-21st Century commercial horticultural context, small is also fragile and may need support from other income streams!

The pandemic may be done and dusted but, by any measure, we’re living in turbulent times. Note to senior management, expect the unexpected! Mind you, we’re not going to run out of customers: over the next 25 years (up to 2050), world population is forecasted to increase by 1.4bn with almost all the extras being in Africa (+920m) and Asia (+450m) and a fair proportion of these will be Moslem or Hindus with meat protein implications to mull on for those in pork and beef. The European and North American share of global population will have shrunk from 17% to14% of total. Globally, average total food consumption is increasing by 6.5kg per person per year but, like the expected population increase, it’s not well spread out: 10% of our world are seriously under-nourished whereas 20% are obese and, in North America and much of Europe , 40+% are as round as puddings and are an unnecessarily “heavy weight” on our health systems. Plant foods – cereals and vegetables – top the food league table, although meat, dairy and egg products are global favourites where they can be afforded.

Focusing on meat, ALL the major meats have seen market growth over the past decade or more, but chicken continues its inexorable growth in global meat market share, usurping pork in 2017 to account for 40% of all ‘land-based meat” consumed in 2024. The “minor” meat lamb accounts for 5% of total with beef holding on to 20% or so share. Oddly, meat statisticians and “Big Meat” internationally, often, don’t appear to consider seafood as being a meat protein choice for consumers, yet fish & seafood are preferred options in much of Asia and Rabobank forecasts that seafood will contribute the largest gains in global protein supplies in 2025 and on, dethroning poultry as the growth leader. The future of plant-based “mock meats” and cell-based meat? Clearly, the former are on the downward curve of the “Gartner Hype Cycle”, not surprisingly as consumers thought early versions tasted dreadful, were expensive and had worrisomely long ingredient lists. Cell-based are past “peak excitement” albeit are continuing to attract venture capital with a longer-term view. Research colleague Miguel asks me “when will cell-based meats attain commercial scale and be on the shopping list of a proportion of consumers?” and my stock reply is “Not in my lifetime ….. (sigh of relief from commercial carnivores) but then, I’m not in the first flush of youth”!

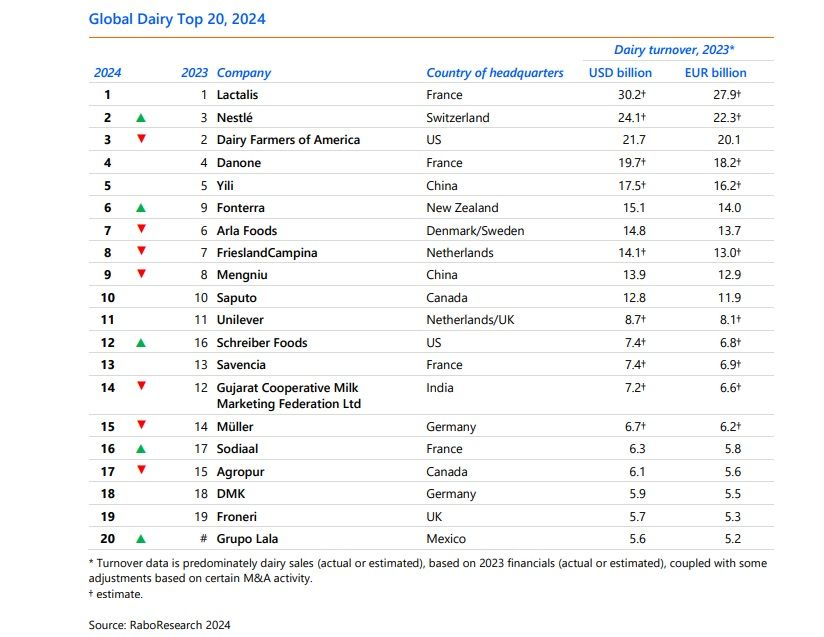

Global dairy is chugging along nicely (dairy products are the world’s 3rd most consumed food group) but their consumer use has been changing rapidly. Plain milk, in a bottle or pouring on breakfast cereals, is yesterday’s use, whereas quaffing a dairy protein shake and woofing down a mozzarella-wrapped pizza is à la mode for Gen Z and Millennials worldwide. The Top 10 of the global dairy processors are advancing at pace, via acquisition, and for good reason – processors with sales of $600+m are up to 50% more profitable (EBIT) than smaller fry.

The egg industry future looks similarly rosy to dairy, notwithstanding the scourge and challenges of Avian Influenza. Scale and profitability are important here, too. The USA egg market leader, Cal-Maine Foods, has revenues of $3+bn and collects eggs daily from 45m hens, making this one company larger than the entire UK egg industry. “Kong Meat”, Brazilian giant JBS has just poked its nose into the egg industry through an acquisition making it the largest egg producer in South America. If you want to see excitement in the out-of-home egg market globally, go to Asia where eggy products have long been firm favourites. Try a yummy Korean branded “EGGDROP” sandwich. It’s in Southeast Asia where innovation in food is buzzing. The region has modest population growth (increasing by “only” 55m by 2033), but household income is galloping along relative to slow growth Europe which is indicative of expected strong future demand for livestock protein products.

What of the future of sustainability of global food production? Around the globe, consumers are increasingly conscious of what they put in their tummies has a profound impact on their own health and the health of our planet. Skimming past a range of hugely important global human health issues, the relatively recent arrival of AOMs – new acronym – anti-obesity medication is starting to cause early and frantic stirs of concern on some food markets. AOMs have certainly taken the attention of big FMCG players, smarting over being sat on the UPF (ultra processed foods) naughty step by food nutrition evangelists. Survey results show that AOM users tend to cut back on snacks and fizzy drinks and increase their intake of healthier protein foods which is good news for those producing meat, dairy and egg products.

In January, The World Economic Forum published its annual global risks report for 2025. Looking at the Top 10 risks over the next 10 years, WEF identified environmental issues as the top four most likely to have an impact on business, viz. extreme weather events, biodiversity loss and ecosystem collapse, critical change to Earth systems, and natural resource shortages. In general, and around the globe, consumers recognise that we’re running out of time to fix the problems that could destroy our world. However, saying this and then doing something about changing their purchasing behaviour and, say, reducing in-home food waste and improving recycling is another matter (the “saying but not doing” conundrum). Barriers to consumers shopping more sustainably include perceived expense of “green” products, difficulty in searching for them amongst the thousands of grocery items on supermarket shelves, lack of knowledge about what is best to buy, dissatisfaction about the efficacy of some “green” products, concerns that “big business” claims are, often, simply “greenwashing”, and “I’m too busy and worried about the food bill/my mortgage/rent to worry right now about sustainability ”.

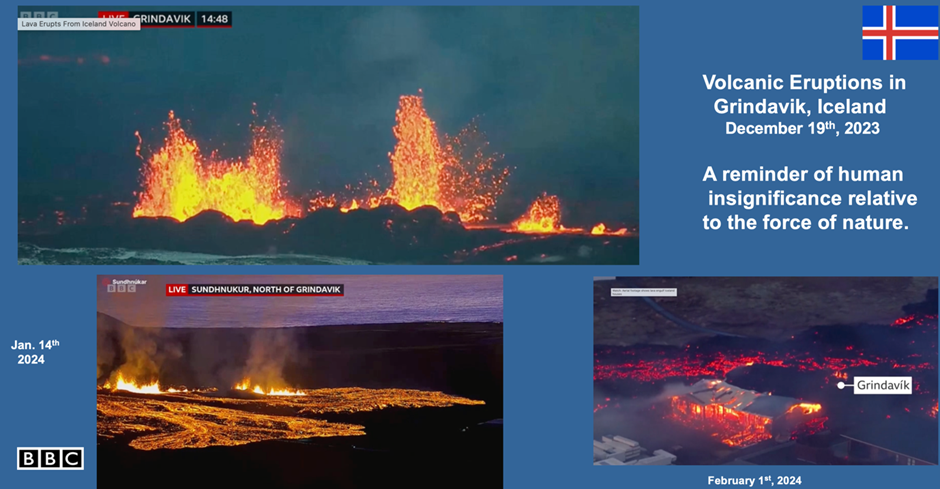

Last year (2024) was the first calendar year that our world reached, indeed exceeded 1.5 degrees Centigrade above the pre-industrial levels and it was no blip! Is it hopeless and we’re doomed to a hellish hot future through inaction? No, although we better get a move on. In 2025, the 30th annual UN Climate Change Conference (COP25) will be held in Belém, Brazil. Back in 2015, most national governments signed a promise to undertake actions on reducing our carbon impact, halving food waste, etc. by 2030. You don’t have to stand on a chair to see 2030 from here and leading “developed nations” are nowhere near delivering the environmental outcomes promised. Yet, the manifestations of global warming are increasingly self-evident (e.g. January 2025 was the hottest January on record) and responsible governments recognise that “needs must” or we will irreparably damage the future of our countries. Try and explain inaction to your grandchildren! Forward-thinking governments are grasping the nettle (e.g. last year, Denmark confirmed the first carbon tax for its farmers) but it can come with a political sting – note Dutch livestock farmers furious response in 2023 to the threat of being forcibly purchased in order to cut Dutch nitrogen emissions which led to the fall of the government and sharp swing to the right in a shock national election .

In the marketplace, smatterings of meat, dairy and egg products are on-shelf with methane/carbon-reduced labels. The principal retail vendors of most countries’ grocery products, the large supermarket chains, have like their governments made promises, too (e.g. Tesco – carbon net zero across its full value chain by 2050). Contentiously, mind you, because such promises largely relate to reducing Scope 3 emissions which account for the lion’s share of the environmental impact along the food chain and these principally relate to activities on individual farms. Thus, the substantive actions to edge towards carbon net zero must and will be made on farms led by those who are trialling improved management and agronomic techniques, supported by businesses in the vanguard of developing low carbon farm inputs, and accelerated by blisteringly exciting technology such as AI and gene editing. How and when this will all happen is for others more qualified to tell. But, for certain, fast forward a decade from now and livestock products and livestock feed will have significantly lower “Enviro Scores” than they do now.

Around the globe, commercial agriculture is simply increasing in scale. The investment cost to be at the leading edge of food production has accelerated through this decade and will continue to do so. A big green grain combine can cost £1m/$1.25m! Fewer and bigger is the farm business trend across livestock and cropping. Mid-20th Century saw the global “Green Revolution” fuelled, in part, by significant public sector funding (national governments and World Bank) but as we fast forward through the present “Technological Revolution”, private sector funding is dominant and there’s a substantial entry cost for those food producers who wish to be on board. Where does that leave smaller-scale farmers? Scrambling, as ever! For consumer-friendly smaller-scale farm businesses, niche markets which could be local and/or for specialty food products can be attractive if the farm “offer” is accompanied by compelling stories about provenance, family history, production process, etc. Many will certainly require, where and if available, policy support to provide them with income opportunities through “greener” farming, as per in England with its Environmental Land Management payments (aka ELM “public monies for public goods”), more sympathetic planning regulations such that they can diversify into tourism (e.g. glamping) and other non-farming activities (e.g. storage, small-scale industrial units) and, for some, just working “off farm”.

Globally, the future for meat dairy and eggs does seem bright notwithstanding that our world is turbulent – politically, socially, economically and environmentally. In regions where incomes and protein consumption are relatively high, population growth is low and notably ageing (e.g. Europe, North America, China) expect to see flat growth in total demand as portion size diminish but frequency of consumption remains at current levels (consumers are simply fond of meat, dairy and egg products and are very reluctant to give them up!). Consumer concerns about the environmental impact of producing and eating livestock products will soften as the livestock industry responds with lower carbon impact products. Where meat and dairy consumption is low and household incomes are low but rising quickly expect to see significant market growth. Consumers in such regions are environmentally conscious, too, not least because they are often in parts of the world that are most susceptible to damage from climate change. Farm livestock are huge emitters of greenhouse gases and, globally, if we don’t manage a significant reduction in their GGEs our grandchildren will be eating less livestock protein!

There’s 8+ billion people in our world and most eat meat – across the globe, average meat consumption is about 45 kg. per capita. By, 2050, we’ll have added another 1.5 billion food consumers, most living in Asia and Africa, and a good proportion of these will be carnivores of some description. Flick through the media and it’s easy to take the view that we’re at “Peak Meat” but that’s far from the case. Global meat consumption has ticked up by about 5 million tonnes per year over the past decade – that’s 0.5kg extra per year on every plate. Mind you, we’re eating more per person of everything (which is a worry for the burgeoning billions who are obese and sadly only aspirational for the close to 1 billion humans who are severely under-nourished) whether it be cereals/grains, fruit/vegetables/root crops or dairy. For meat, the average figure masks the fact that the level of meat consumption is linked closely to level of family income (and, for some countries, religious practices). Well-heeled USA consumers woof over 100 kg. of meat per capita, whereas in, say, economically struggling Burundi the figure is a mere fraction of this, and 30+% of the huge, expanding Indian population eat no meat at all.

In this short article, only meat from livestock grown on land is considered. Thus, there is a gaping hole because we’ve parked fish and seafood! Across Asia, fish are a huge proportion of total meat consumption (e.g. in Japan, Indonesia, Malaysia, Hong Kong), as is the case in some European countries such as Norway, Iceland and Portugal) competing directly for the household purse with beef and pork, for instance. For land-based meats, the global story has been the disruptive impact of poultry on the meat industry, principally broilers, over the past 60 years: in the early-1960s, poultry meat consumption was around 3% of global meat total, with the principal spoils shared between pork and beef; ten years ago, the transformed picture showed pig and poultry meat sharing 74% of meat consumption; but, by 2024, poultry’s seemingly inexorable rise has given it a 40% global meat consumption share, with pork on 34% and beef slipping down to close to 20%. Sheep and goat meat, always minor on a global basis, have seen their share slip from around 10% in the early-1960s to 5% by 2024.

So, to paraphrase Mark Twain, the reports of the death of meat have been greatly exaggerated! Yet, the progression of meat consumption depends, inter alia, on country, demographic trends, livestock species, and time period being considered:

take voracious USA, for example: in the mid-1970s, per capita beef consumption was 40 kg. (88 lbs.) but, now, it bobbles along around 25 kg. (with short-term trends depending on the state of the cattle cycle, spikes in beef retail prices, etc); at 23 kg., pork per capita consumption has been relatively stable for some decades, again like beef, hiccoughs largely being related to hog cycle movements; the market for lamb shouldn’t be dismissed but, frankly, at 1 kg. per capita, cayotes are the biggest lamb consumers in the USA; and it’s poultry, principally broiler consumption that has driven overall American consumption to its present stratospheric levels – in the pre-1950s, at 5 kg. per capita chicken and turkey were for Christmas and, now, at 50 kg. “Chicken is for Tonight” (with apologies to brand owner Simplot)!;

Australians are as carnivorous as Americans, with meat consumption per capita above 100 kg. and the overall picture isn’t too different – beef and lamb consumption is in slow decline and the total meat figure is maintained by modest growth in chicken consumption;

relative to the above gargantuans, at around 60 kg. per capita, the British are more modest even wimpish in their meat consumption, albeit with a similar pattern to the above – i.e. beef, lamb and pork consumption drifting lower through time as poultry flaps up! During the current “cost-of-living crisis”, beef and lamb, as the premium-priced meats, have been under pressure. Yet, analysing UK “Family Food Survey” data (i.e. measures of food quantities eaten in the home) rather than more aggregated supply disappearance measures, to use a currently popular phrase, a more nuanced and concerning (from a meat industry perspective) picture emerges. In-home total weekly meat consumption per capita has decreased from 1060 grms. in the early-2000s to 920 grms. in 2024 (a 10+% decline). Consumption of all meat and processed meat products declined most recently (price pressures) but, through the past 40 years or so, the strongest growth category by far was for pies and ready meals which doubled through this period. This isn’t surprising and we’ll address it briefly later;