Farmers are often grumpy. It’s the unpredictable elements of their business such as tussling with the vagaries of the weather, market prices, awkward customers and regulators, and coping with the peccadillos of their neighbours and wayward countryside visitors. But, right now, they’re angry even furious all around the world. In India, farmers are marching on Delhi. Across Europe, capital cities are under siege. What’s it all about?

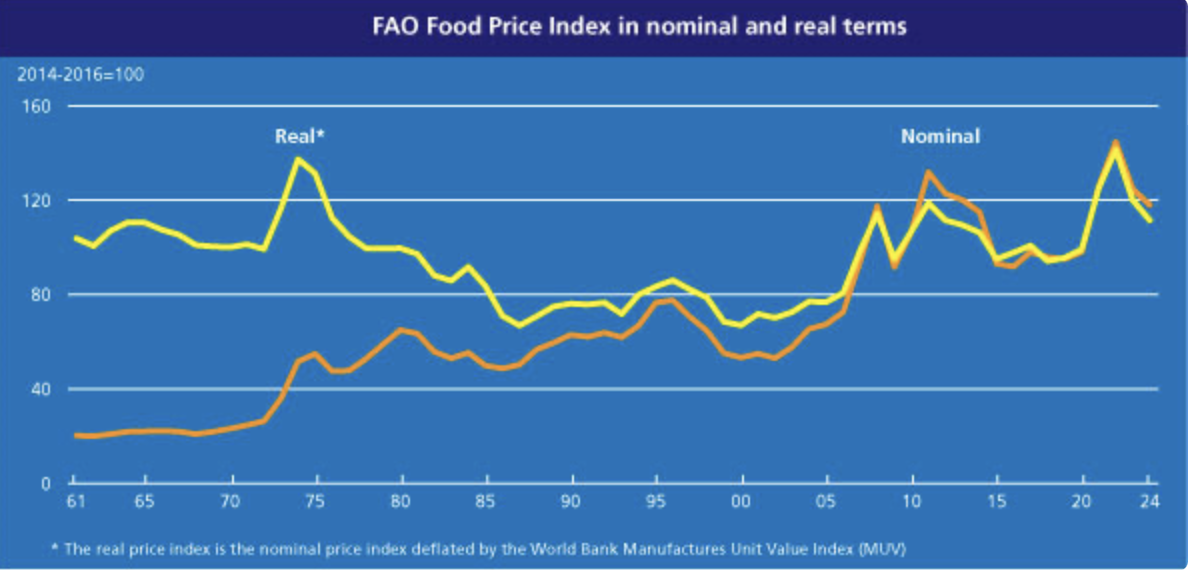

In history, whenever we have consumer food prices spiking, we look for the villain. The first port of call is generally the supermarkets, followed by the big, branded food processors. Global food commodity prices peaked at record levels in March 2022 but it took a few months for these elevated commodity prices to work their way through to higher prices at retail. In the UK, food price inflation spiralled up to just under 20% (year-on-year) by March 2023. Since then, the rate of food price inflation has declined every month to a “modest” 7% in January 2024 – a level that would have been labelled “Shock, Horror” by the tabloids in the balmy pre-pandemic period. So, if food commodity prices were burgeoning, why would farmers be revolting? Well, commodity prices have declined by 25+% since their giddy heights and, concomitantly, key farm input prices (e.g. fertiliser, energy, finance, herbicides, seeds, etc.) have come off their highest levels but remain well above those that were the norm prior to the calamitous past four years! This has resulted in severely squeezed margins for many farmers.

In terms of angry farmer responses, who’re the most revolting? We’d put Indian and European (EU) farmers in the top spots, normally conservative New Zealand cockies in bronze medal position, Scottish and Welsh farmers mid-table (outraged about policies directed at non-food use of their land), with English farmers lower down the angry league table being a more circumspective “jolly cross”!:

- close to 60% of India’s 1.4bn population rely on agriculture for their livelihood. There are 120+ million farmers and 85% of them sit on tiny pockets of land. Heavy duty policing has stopped thousands of farmers marching on Delhi (as they did in 2021 and they stayed there for an entire year) but, likely, their progress to the capital is far from over as farmer leaders have just rejected a government proposal to buy selected crops – pulses, maize, cotton – at assured prices on a 5-year contract. The farmers are hell bent on gaining a similar deal for all of their crops;

- farmers across Europe have taken to the streets in Poland, Czech Republic, France, Germany, Spain and Italy to fight low prices and high costs, cheap imports exacerbated by Autonomous Trade Measures (ATMs) introduced to give Ukrainian cereals and oilseeds access to export markets via the EU, and EU climate change constraints (e.g. EU Green Deal). The EU Commission’s response to this farmer pressure has been to dilute its climate change goals – e.g. the EU 2040 Climate Target no longer mentions a 30% cut in non-CO2 emissions from agriculture, such as methane emissions from livestock and nitrous oxide emissions from soils;

- in New Zealand, livestock farmers united to dismantle the incumbent Labour party’s climate policies and, with infuriated urbanites, contributed to the Labour Party’s ejection and a significant political move to the right in the October 2023 election;

- in the UK, Rishi Sunak became the first British Prime Minister in 15 years to address the National Farmers Union Conference offering £220m ($275m) to put into new food productivity schemes focussing on farm technology and automation to reduce reliance on overseas workers. He proffered plans to reduce red tape and make it easier for farmers to diversify their businesses. Farm to Fork annual food security summits have been promised and he assured farmers of milk, pigs, eggs, chicken and fresh produce that regulations would be introduced to ensure fairer contracts for them with their major customers, particularly those iniquitous supermarkets.

Is this democracy in action – caring governments listening to much respected rural members of the electorate and providing solutions to farmer problems? Maybe but it’s worth noting that India, the European Parliament, and The UK all have key elections in the next few months raising the likelihood of government leaders responding sympathetically to the rural vote! The UK Government response is welcome but not of the same order of that emerging in India and the EU where firmly held principles – in India on accelerating structural change in farming, and in the EU on its much-vaunted Green Deal – are being/will be sacrificed to mollify angry voters. It was ever thus – the squeaky wheels get the grease!

Elections will be held, some governments will change, farm input and food output markets may stabilise in the short-term as we judder our way through the remainder of this decade. However, the global picture is far from being a haven of tranquillity and it’s most unlikely that the international food commodity price pattern which followed that of the August 1973 price peak (the nearest equivalent to our most recent March 2022 one) will be repeated. Back in 1973, analysts opined that the price peak would usher in much higher food price levels than in the past. In fact, over the next 30+ years (1973-2005), international food prices trended downwards (a halcyon period for food consumers), as global food supply flourished through farmers improving management techniques and increasing the use of fertiliser, improved hybrid seeds and herbicides.

Over the next 30+ years from our most recent 2022 price peak, international food commodity prices will be substantially more volatile than in the past. Overwhelmingly, commodity price instability will reflect some combination of increasingly extreme “climate events”, oil & gas price spikes not least linked to international political instability, government biofuel policies as green target dates come closer and domestic “energy security” concerns rise (note the recent impact of India’s domestic biofuel policies on the world sugar market), and disruptive changes in national food exporting policies – such as India’s ban on selected rice exports and Turkey’s ban on bulk olive oil exports. From a farmer perspective, this will require substantial resilience, traditionally, a farmer strong suit, but also, the technical and financial capacity of farm businesses to incorporate the new technologies that will be central to profitable green farming in the 2030s such that we can produce more food with less impact on the health of our planet.

Will the angry exchanges between farmers and their governments continue through the remainder of this decade? Very likely, YES! Under the auspices of the United Nations, most governments have signed up to the target of reaching “Net Zero by 2050”. In COP28, completed in December 2023, a global roadmap given the thumbs up by 130+ countries was released by FAO showing the pathway for global agriculture and food to make its contribution to achieving Net Zero without allowing global temperatures to exceed 1.5C above pre-industrial levels. Yet the EU has stumbled at the first hurdle by diluting its climate change goals, notwithstanding that the EU has already signed up to cutting gross GHG emissions from agri-food systems by 25% by 2030 and to be CO2 neutral and make significant cuts in nitrous oxide and methane emissionsby 2035. You can see 2035 from here! It’s not as if EU farmers are being asked to support these green initiatives for nothing. After all, one-third of the massive EU annual budget goes to farmers, most in the form of direct farm subsidies. Looking at the farm support schemes in the EU (and the UK for that matter), Kiwi farmers must be shaking their heads as they “celebrate” the 40thanniversary of the subsidy rug being pulled from under their feet. New Zealand is a signee to the UN (FAO) Global Climate Change Road Map and the promises it has made will be delivered by its farmers largely off their own backs.

One of our principal reflections on the recent flurry and expected continuing angry exchanges between farmers and their governments is that it is indicative of lack of collaboration. High profile international events such as the COPs leading to reassuring pronouncements on a better future for our planet are more likely to be successful if they are based on firm agreement with those who must deliver the promises made, i.e. those that actually farm the land or ocean! Finally, the above views on farmer anger do not cover those producing fresh foods for sale principally via supermarkets. That’s another story and, very shortly, we’ll offer a few thoughts on this contentious topic.