The USA is a Big Beast in geographic size, population and economic and political clout. Back in 2020, spurred by the Conservative Government’s desire to be seen as a nimble, swashbuckling free trader unencumbered by sclerotic EU bureaucracy, negotiations were started to establish an FTA (Free Trade Agreement) with the USA. Progress stalled, like many trade negotiations, but it’s mooted that the President/PM of the respective nations are determined to have something on paper before the upcoming elections. After all, the USA and UK are significant trade partners – USA exports to UK are around $77bn and UK exports to USA are $65bn. In history, food and drink trade between the two countries has been modest: the lion’s share of UK exports being Scotch whisky, then, other spirits, beer and salmon; with wine, tree nuts (e.g. almonds), and bakery goods leading the charge from the USA. Yet, the UK agricultural sector is hugely apprehensive of an FTA which includes comprehensive coverage of food items from the USA. The apprehension has been fuelled by the swift FTA trade deals that, to the fury of UK livestock farmers, were swished into place between the UK and Australia (2021) and New Zealand (2022) and the expectation that we may well complete agreement to join the CPTPP, an Asia-Pacific trade bloc, in the latter half of this year. It’s a good time to peek at the USA from a farming and food perspective just in case normally glacial trade negotiations grow some wings! Whilst the UK has “a special relationship with the USA”, it’s propitious to keep in mind that our prospective free trade dance partner is elephantine so watch your toes! Attached is a series of slides that give the detail of the following commentary.

Give or take, the USA has a zero-trade balance on agricultural trade – exporting around $200bn and importing roughly the same, whereas UK has a significant trade deficit on agricultural, food and drink – we export $31bn, with whisky and salmon from Scotland in top spots, importing $73bn, not least fruit and vegetables from Europe. American agri-food exports are dominated by 4 categories – grains and feed, oilseeds and their products, fresh produce (large exports of fruit and vegetables to Canada in the colder seasons), and meat (principally, beef largely destined to Japan/S. Korea and other Asian markets and pork). The key agri-food export destinations are China, Mexico, Canada, Japan and (lesser so) the EU. These same 4 categories dominate agri-food imports to the US, with horticultural produce the largest (e.g. fresh produce from Mexico counter-seasonally). The US is a substantial meat importer – beef from Canada and New Zealand, sheep meat from Australia, pork from Canada.

What about the USA food production sector – are all farms Texan size?! Average farm size is 180ha (450 acres) more than double the average English farm size. The US has 2 million farms on 364m ha. (we’ve got 200,000 or so on 17.2m ha). “Small” family farms (gross cash farm income <$350K, i.e. £275K) comprise 89% of all farms but account for only 18% of production value. The large family farms and corporate farms account for 5% of farm numbers but 63% of production value. Many of the “small guys” are essentially hobby farmers and much of their income comes from off-farm sources. Corn and soybeans dominate grains and oilseeds production with an 87% share of land. 90% of soybeans are used for livestock feed, whereas 45% of corn is used for livestock feed, 44% for ethanol production and 10% for human food (with a third of this being converted into HFCS). In stark contrast to the UK, more than half of US cropland is sown with GM seed: essentially, all the area for corn, soybeans, cotton, canola, and sugar beet.

As an aside, the US crop seed sector has undergone significant structural change, spurred by the expansion of intellectual property (IP) rights and heavy-duty investment in R&D by the major seed companies. Bayer and Corteva GM seed accounts for 72% of planted corn area and 66% of planted soybean area in the US, in addition Syngenta is a significant but “minor” player. The “Big Four” (the latter 3 plus BASF) invest around 10% of their seed and agrochemical sales value on R&D to deliver improved yields for farmers and secure, profitable IP for themselves! Between 1990 and 2020, prices paid by farmers for “generic” crop seed increased by around 170%, and IP-protected GM seed prices rose by 463% – compared with a 56% increase in crop commodity prices over this period.

Apropos concentration in the crop seed market, a similar picture emerges in meatpacking industry in the US: 4 firms, Tyson, Cargill, and 2 Brazilian firms JBS and Marfrig account for 85% of beef processing; WH Group (Chinese-owned), JBS and Hormel account for 67% of the hog/pork processing sector; and JBS and Tyson account for 45% of chicken processing. Concentration in these sectors is high and has been rising. The names of the major players are not unfamiliar to livestock and meat participants in the UK and elsewhere! Encouragingly, in the USA, rising meat price spreads/packer profits is attracting new entrants into the meat processing industry providing livestock producers with more selling options than simply the “Big Boys”.

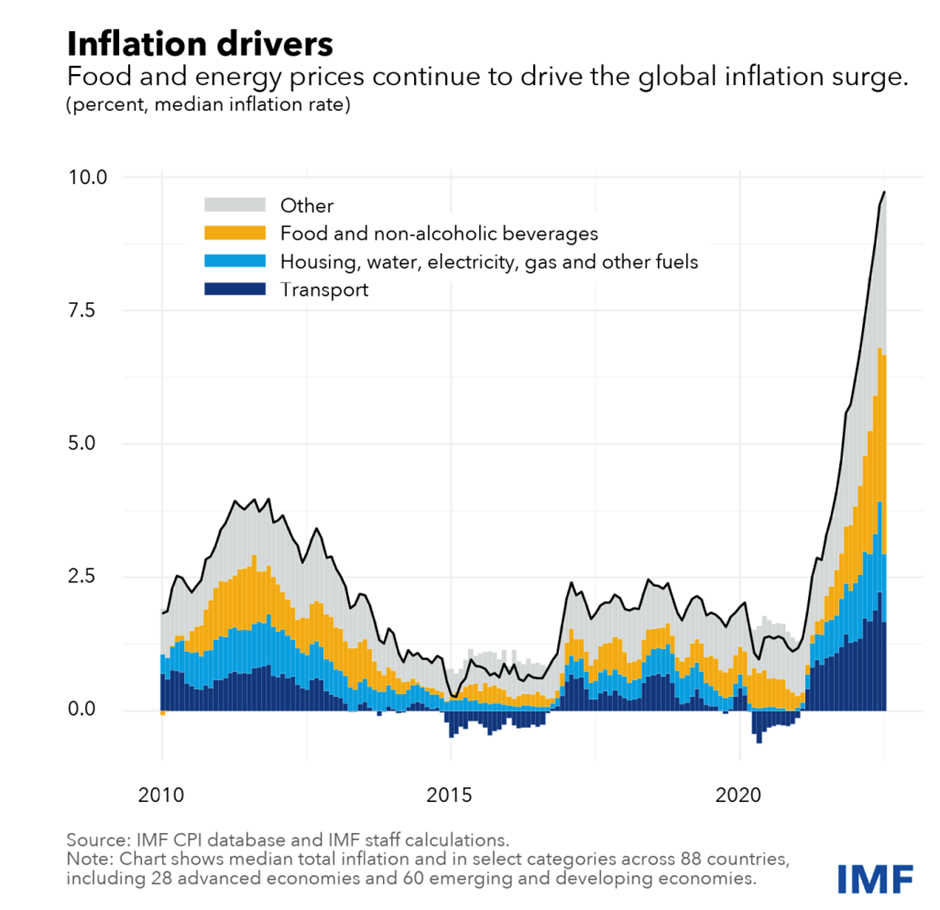

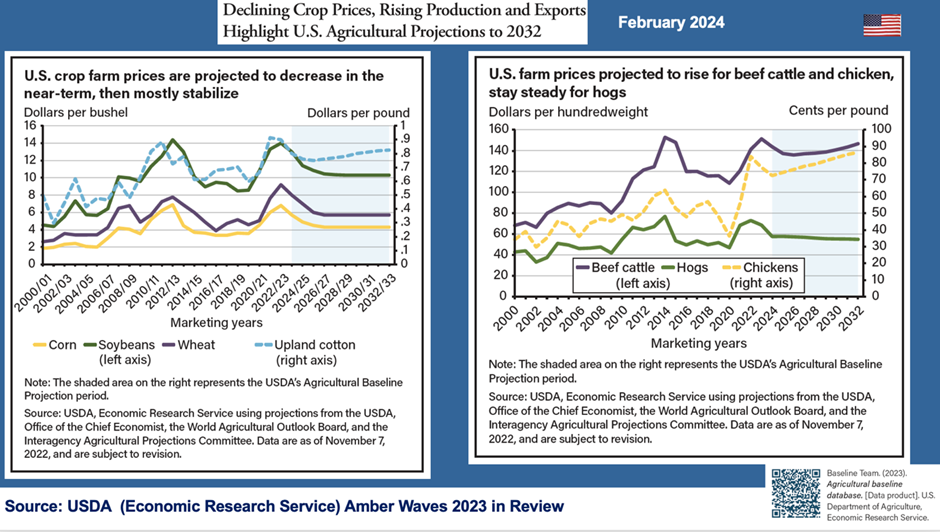

What of the USDA’s view on future production and prices for crops and livestock through the remainder of this decade? Corn and soybean production and exports are expected to show strong growth and exceed record levels, whilst crop prices are projected to decline in the next 3 years and then generally stabilise. This isn’t great news for crop farmers as margins will be under pressure. Whilst global fertiliser prices returned to 2021 levels in later months of 2023 after surging in 2022, their 2024 and expected future levels are still substantially above those of early-2021 and all other farm input prices are at historic highs. Fertiliser “security of supply” continues to be of concern with Russia and China accounting for 25% of global fertiliser trade. Production and exports of beef, chicken and pork are projected to increase over the next 10 years. Beef and chicken prices are projected to remain elevated while hog/pig prices are forecasted to fall.

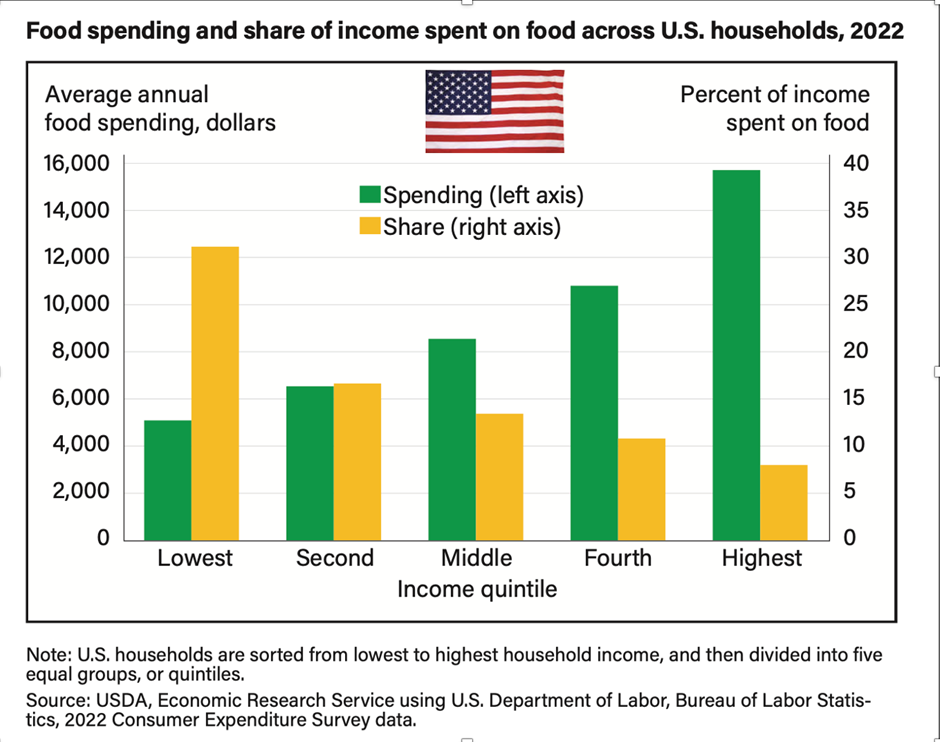

Who gets what from the “Food Dollar” in the USA? Roughly one-third (34%) goes to food services – in the US, over 50% of consumer spend on food is “away from home”, whereas this figure is around 40% in UK. Food processors take 14% of the food dollar, whilst 12% goes to the food retailer and the wholesaler takes 11%, with the beleaguered farmer, the producer of the raw ingredients, taking a lowly 8%. Just as in the UK, consumer household income has become increasingly polarised in the USA: families in the lowest income 20% spent $5,000 on food ($100/wk) in 2022 accounting for a good third of their annual income. The well-heeled in the top 20% of income spent close to $16,000 on food for the year ($300/wk) accounting for around 7% of their household income. For low income households , there is substantial income assistance for food from the state: in 2023, this was close to $150bn – most via SNAP, the Supplemental Nutrition Program, supported by Child Nutrition Programs and WIC, the Women, Infants and Children Program.

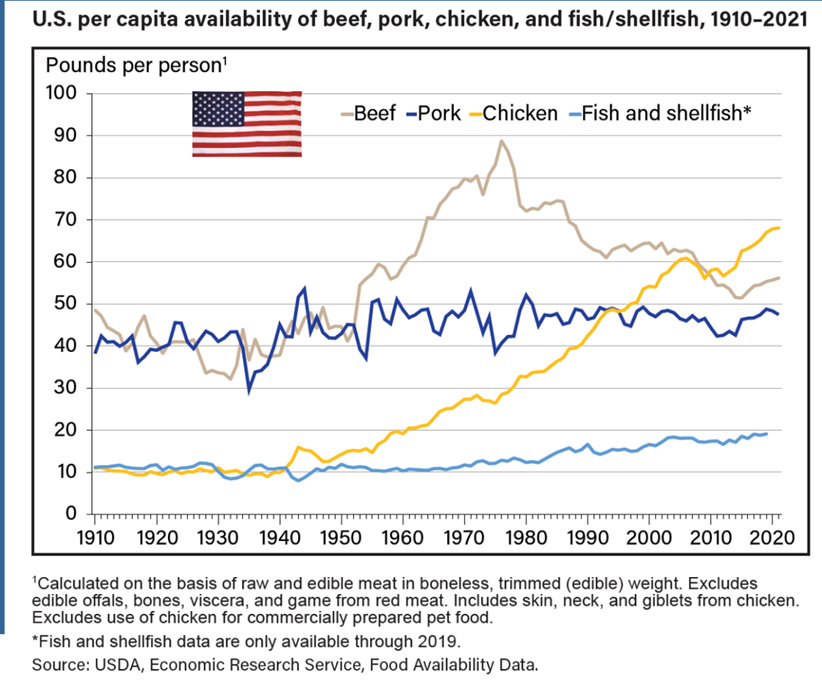

A short note on meat – Americans are notably carnivorous! The figures presented are for boneless, retail weight meat and, excuse us, are in lbs! For the past 50 years, per capita beef consumption has wended its way down from close to 90lbs to near 50lbs in the early 20teens but has recovered of late to closer to the mid-50slbs. For 75 years, pork and its products has meandered around the 50lb mark. Like in many countries, chicken has been the meat industry disruptor reaching near 70lbs of late. Over the last 50 years, fish consumption has slowly increased to its current level of 20lbs per capita. What about veg.? Through the past 20+ years overall per capita consumption has trended downwards. Starchy vegetables, particularly potatoes, are of huge importance albeit slowly declining year-on-year and processed potatoes (frozen predominately) continue to replace fresh. Fresh and processed tomatoes have maintained their prominent position, and “other red” and orange veg. (e.g. red & orange peppers, carrots) have seen consumption growth, as has pulse consumption (chickpeas, lentils, peas, beans), particularly in more recent years.

A last word on food consumption, Americans are eating too much and, often, with unhealthy diets. The adult obesity rate is 42%. It’s lower for children but increasing at an alarming rate. Very recent research identifies that average proportion of calories from protein in the American diet decreased from 14% in 1961 to 12.5% in 2000 with more calories from fats and carbohydrates making up the difference. For sure, they didn’t eat less meat. Many reached too frequently for the snack box and over-ate addictively moreish food products that, most recently, have been labelled Ultra Processed Food (UPF). Americans are not alone! The obesity crisis is global with terrifying consequences for global consumer health, pressure on medical services and global productivity and economic growth.

Enough already! The previous thoughts are provided to give the reader an overview of some aspects of food production and consumption in the USA. In this final brief section, we’ll look at what the implications might be for UK farming and its food industry if an FTA was agreed between the 2 countries. Might this happen in 2024? The PM and President of the 2 countries both need quick wins in this election year and, to use NFL parlance, could elect to use a “Hurry-Up Offense” approach to trade negotiations. Would this bring opportunities or threats for UK agri-food & drink?

First, let’s be positive! The USA is a big, rich country with plenty of high-income consumers who know and like us. They’re gaga about our Royal Family and historic buildings, and assume we largely dine on fish & chips. The Scots would be ecstatic, and exports of whisky and salmon would soar in a tariff-free market. There are considerable opportunities for our specialty cheeses, pork and lamb.

The big negatives for the UK in a US trade deal relate to concerns about “low standards” in the USA regarding animal welfare, the environment and more contentiously, food safety (e.g. the emotive American chlorinated chicken issue). From a UK farmer perspective, the rub is that being in the van on welfare and the environment brings additional production costs and it’s simply unfair if competitors can enter our market without matching our mandatory regulated standards. These concerns – being on the cutting edge on green issues but, also, on “the bleeding edge” – are shared by EU farmers.

Animal welfare regulation in the USA is complex and slow (relative to the UK). There’s no national policy relating to farm animals as it’s a state responsibility with 14 out of the 50 states already started on the welfare journey. Liberal California is way ahead with cage-free eggs and veal and a ban on sow gestation crates already in place. As of now, the UK pork sector has a “gateway” into the Californian pork market with the state’s Proposition 12 certification (via NSF). Animal welfare regulations and some agri-food businesses are moving albeit slowly in a direction we’ve long embraced in the UK: e.g. by 2026, 17% of breeding sows will be gestation crate-free; and McDonald’s has met its cage-free pledge on eggs this February, some 2 years ahead of its initial plan. Beef produced with anabolic hormones will be a trickier trade issue as 90% of beef cattle produced on USA feed lots have such implants. The biggest barrier to “hormone beef” imports into the UK is that our shoppers are vehemently antagonistic to such! Although, in the unlikely event that a trade deal gave such beef the all-clear, it could be squirreled into the lower end of the food service market where product transparency and labelling are less in evidence.

Environmental considerations relating to agricultural production will be integral elements in any future global trade agreements and should be included, albeit contentiously from a USA perspective in an FTA with UK. Take note of EU farmers demonstrating against the pace of introduction of The European Green Deal. Just imagine the UK farmer reaction if, in a trade agreement, the partner was given carte blanche to use practices and products banned on their farms – they’d be incandescent with rage! The direction of travel on environmental constraints to those importing products into the EU is clear: EU Deforestation Regulations require companies trading in cattle, cocoa, soya, oil palm, coffee and wood to prove that their production did not result in deforestation. The UK is on the same track and if, for example, some pesticides are banned on specific crops it would be hugely controversial if farmers in trade partner countries were allowed to use them on products which end up in our own country. Right now this is a huge issue. The UK is a significant food importer. Indeed, the land used “offshore” to produce the food we import is close to the same area that we produce food on at home! We can’t be holier than thou at home if we are exporting environmental problems to our trade partners supplying us with our food!

Completing an UK-USA FTA in this calendar year would be a Herculean task and one not supported by many in UK agriculture. If it came to pass, would our food market be swamped with American fare, and would it be a halcyon period for UK food exporters? No! Apart from anything else, building a market presence with new customers takes time. Most likely, the current pattern of trade between the two countries would continue but in greater volumes and values. Finally, through the past few turbulent years, concerns about national food security have been increasingly evident. Likely, our political masters, enthusiastically encouraged by UK farmers, will be more focussed on increasing food production at home than on forging international food partnerships.

For those fond of stats. related to the above, click on the following link: