Every January, two hardy perennials burst into full flower. Here’s a brief botanical review of them both.

Established in 2014, Veganuary is native to the UK but, wind-borne, its seeds have germinated in dozens of countries and has a mission to inspire people to “try vegan”. As “A Movement”, Veganuary carries an implicit health warning for carnivores and livestock producers. Smart marketing is at its core: in January, we’re predisposed to try a healthier diet; plant-based foods are firmly on-trend; trying vegan food for a month gives us a guilt-free opt out after only 4 weeks (“tick, done vegan!”); the promotional material doesn’t focus on killing distressed animals, rather on “saving” cute, cuddly ones; certainly, in the UK, the food media and food retailers of all stripes are supportive – e.g. hard discounter Lidl (not the immediate grocer of choice for the urban élite chattering classes) has “Going Meat-Free in January?” as the strapline of its New Year adverts; and, particularly, post-COP26, it’s consonant with the notion that family food purchase choices can contribute to saving the planet.

Vegan and vegetarian diets have market traction in many higher income countries (they’ve never lost it in emerging countries where meat is still a relative luxury food) and the proportion of the population claiming that they follow vegan or vegetarian diets is edging up, albeit slowly. Much of the media hype revolves around consumers eschewing real meat and embracing “fake” meat yet, in the market place, this isn’t the case. In the USA, plant-based meat sales have declined 7 months in a row. Plant-based heavyweight Beyond Meat’s Q3 sales were down 16% year-on-year and its share price as of January 3rd 2022 was one-third of its top value in January 2021. Meat substitute products festoon supermarket shelves but sales of many are floundering. What’s the problem? Shock horror! Many fail to deliver on taste and texture, are increasingly perceived to be “over-processed”, are criticised for being unhealthy, not least because of high salt content, and are expensive relative to “the real thing”. European sales of plant-based meats have been rosier. Beyond Meat has provided the patty for the successful launch in the UK of McDonald’s McPlant burger. The USA could be a harbinger of future demand, although, perish the thought, it may be that our continued strong demand for meat substitutes indicates that European taste buds are less refined than our trans-Atlantic cousins.

Tentative although future demand for fake meat may be, venture capitalists haven’t been shy at throwing money in the direction of prospective plant-based unicorn companies – Impossible Foods is purportedly valued at $7bn, although it’s yet to make a profit. It has raised $2bn of development finance over 2 years, and 10 other plant- and cell-based food companies each raised $100+m in 2021. There may be tears before bed time!

Thumbs down for plant-based foods? Far from it, they have excellent market prospects. Tasty, healthy, convenient, affordable plant-based meal and snack solutions are and always have been on the up. The best of Big Food (e.g. Nestlé, Unilever) are investing heavily in the sector through their own NPD and via acquisition, gobbling up nimble start-up companies. Their major competition will come from private label manufacturers for major grocery retailers – Tesco’s Wicked Kitchen and Marks & Spencer’s Plant Kitchen are in the van. Implications for the meat industry? In higher income countries with current high levels of per capita meat consumption, we’ll slowly eat less meat, particularly beef. Those more comfortably off, however, will eat “better” meat and the definition of “better” will be a topic hotly disputed!

Bolting is a term applied to vegetables when they prematurely run to seed. Humans have a tendency to do so, too and are chastised for such every New Year …. and, particularly this year as waist lines expanded after months of working from home accompanied by surreptitious snacking! Our Lock Down promises to eat healthier came to nought in the UK where average weight gain through the pandemic has been 3+kg – 2 out of 3 adults and 1 out of 3 children are overweight or obese and the NHS and tax payer stump up £6bn/year treating weight associated ill health.

The Centre for Food Policy report for the UK Government’s obesity research unit warns that “easy access to and availability of unhealthy food 24 hours a day across the UK makes losing weight difficult for millions who are trying to reduce weight – we eat more because food is easily available and its proximity triggers us to want food more often”. It’s a particular problem for those on low incomes as cheap, unhealthy food is more likely to be promoted in shops and supermarkets. It’s the dark, other side of the coin problem associated with the hyper-competitive UK food retail sector which in most respects deserves applause from consumers for delivering low food prices for food overall, whether it be healthy or unhealthy. Should Tesco be scolded for offering an Aldi Price Match “Hearty Food thin pepperoni pizza for 67p ($0.90)?!

The UK Government has an obesity reduction plan which many view will fail in the face of a perceived junk food culture and where consumers are “bombarded by unhealthy food options”2. Food high in saturated fat, sugar and/or salt and deficient in fibre, protein and other good stuff is broadly defined as junk! Later this year, junk food advertisements will be banned on TV and the cinema (and online) prior to 9pm and promotions such as BOGOFs and aisle end placements of HFSS products will be illegal. Health activists call for fresh fruit & vegetables to be discounted but aren’t they already? Basic fresh produce prices are astonishingly low, just ask any fruit & vegetable producer.

Obesity is as much a pandemic as Covid-19 and removing the problem is as complex. A multitude of factors are key contributors, including: genetics and biology; household income; financial insecurity; deprivation; weight stigma; access to opportunities to be physically active; cultural norms; food prices; portion sizes; food and cooking education; food availability (e.g. food deserts); life experiences; food advertising and promotions; mental health; access to treatment and support.

Global problem although obesity is, its incidence varies hugely – across the OECD countries, 40% of USA adults are obese versus 4% of Japanese adults. In the so-called developed world, food industries should steel themselves for a plethora of government-imposed measures to combat the problem ranging from soft touch bans on food promotions and placement, through mandatory health warning labels on food at retail and in restaurants, to hard-edged taxes on foods high in fat, sugar and salt.

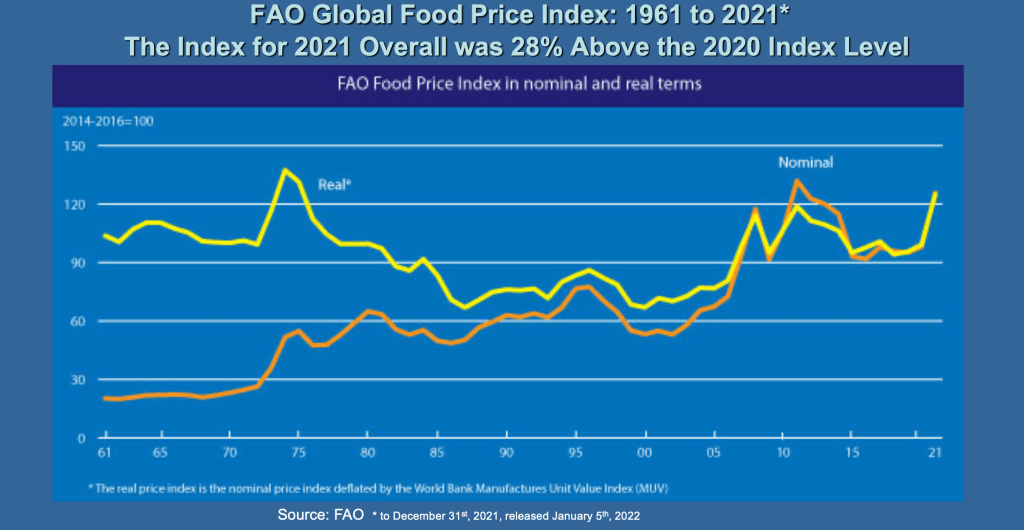

Veganuary will come and go and our promises to reduce our waistlines will evaporate like snow off a dyke. In this first quarter, supply chain disruptions caused by Covid-related labour shortages will cause food industry challenges and irritate pampered consumers. But the global food issue that will dominate the headlines throughout the year will relate to escalating food prices. The FAO Global Food Commodity Price Index for 2021 was 28% above that for 2020 and these food price inflationary pressures have by no means passed through to global retail food prices.

Higher basic food commodity prices are very welcome for farmers but rocketing farm input prices are not! “UK farmers braced for spring fertiliser crunch after prices triple” shrieked The Financial Times, but it’s a global problem and particularly for poor small-scale farmers in the emerging world who produce the majority of the food for their burgeoning population. Fertiliser use will be down causing yields to decline and continued upward pressure on food prices at retail. Container freight rates will remain stickily high for much of the year – we import 40% of our food in the UK! General inflationary pressures abound around the globe – in the UK, household incomes will be under stress as energy prices remain at high levels and tax rates (i.e. National Insurance) increase. Consumers will look to trim their budgets on items on which they have flexibility like food items. Watch out for: full on food retail price wars in many countries; and political turmoil particularly in lower income countries – when staple food prices spike, the huddled masses take to the streets (and even the seeded sour dough and matcha tea brigade get peevish).

We’re set for a rough and tumble, challenging year for those in the food industry and for food consumers. It will require companies and households to be resilient with resilience defined as “the capacity of dynamic systems to adapt successfully to challenges that threaten their function, survival, or future development”. Looking at how largely adeptly the global food system has handled the unwelcome Covid pandemic, we believe the global food industry can cope in spades with what’s coming our way in 2022. Happy New Year!

David and Miguel

January 6th, 2022