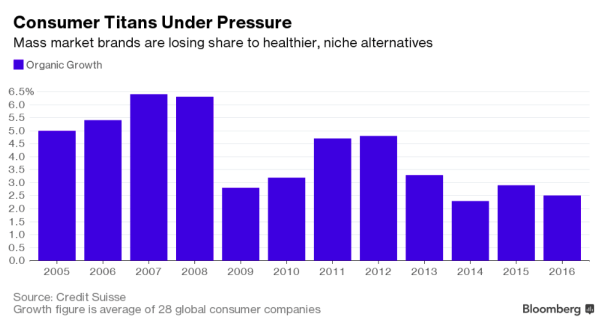

Big food companies haven’t been cracking open the champagne in recent years – in developed markets, sales have been in free-fall, with fast-growing emerging markets saving the day but, still, the overall sales trend has been ominously downwards, and this has been reflected in their share prices. It’s darkly amusing because consumer activist groups still rail against Big Food – Unilever, Nestlé, Kraft, Mondelēz, Danone et al – because, purportedly, they have global consumers in their thrall! But, listen to Emmanuel Faber, Danone’s CEO: “the food industry is going nowhere – because short-sighted companies see only a transactional relationship with consumers, not deeper ones based on values”.

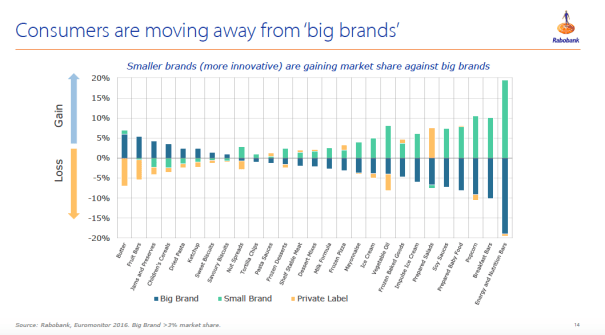

Rabobank graph with Euromonitor data for the US Market, showing the performance of Big Brands, Small Brands and Private Label in different categories.

What are the problems for Big Food? Well, there’s the one Faber identified above and here’s four more:

- Consumers have moved on eschewing “over-processed” foods as they seek healthier, fresher, more natural snacks and meals with simpler ingredients. Take breakfast cereals for example, Kellogg’s Frosties, Post’s Fruity Pebbles and Honey Bunches, General Mills’ Cheerios screamed “sugar-drenched” to mums (if not to kids). Start-up companies, generally, run by millennials spotted the slow-footedness of these ponderous dinosaurs and whizzed in with new age products that pleased parents and their offspring. We blame those pesky, difficult-to-please centennial and millennial consumers. They deserve a good spanking but, the trouble is, there are 4 billion of them worldwide;

- More broadly, consumers have been showing a distinct predilection to trust must less our traditional pillars of society – like big government, the church and, yes, big business (legal but nonetheless dodgy tax avoidance by Starbucks et al hasn’t helped here);

- Big Food’s major customers – supermarkets – are under extreme pressure as Amazon and Alibaba are in the process of changing how consumers shop for groceries. When Tesco gets squeezed, its suppliers feel the pain. Doubly so, when supermarkets expand their private label offer at the expense of branded products to seek points of differentiation. What’s more, the centre of the store is being squeezed as shoppers flock to the perimeter where more exciting fresh and freshly-prepared foods are sold. No wonder the centre of the store is darkly termed “the morgue”!;

- And, of course, an extended deflationary period – reflecting declining raw material prices (corn, soy, energy, etc.), over-supply in grocery retail bricks & mortar, households still recovering from the vicissitudes of the GFC hasn’t been helpful. When inflation is rampant, it’s a tad easier to sneak up retail prices than when shoppers expect prices to remain the same or fall.

Like big business in general, Big Food has this recurring nightmare of exiting the top 100 companies in their respective stock markets. The average lifespan of a company in the S&P 500 was 60+ years in the 1950s and, now, it’s less than 20 years. So, CEOs have similar nightmares to football managers in the UK Premier Football League – viz. the threat of demotion to the lower leagues! To continue the football analogy, food businesses do the same as soccer teams when results turn against them – they change managers! Who’s done this recently? – well, in the last 20 months, 17 CEOs of big food companies have been sacked or “stepped down/retired”, including Kellogg’s, Mondelēz, General Mills, Hershey and, God forbid, even rock solid Nestlé. Particularly for US companies, getting the boss to fall on (usually) his sword is the first move to convince investors that a turnaround is a coming (shackled as they are to “deliver the financial numbers” every quarter). So, being promoted to CEO is akin to being presented with the “Black Spot” in Robert Louis Stevenson’s classic “Treasure Island” – the pirate king is doomed to a tragic end!

Sack the boss, is that the solution to its woes? No, Big Food has other arrows in its turnaround quiver, like:

- Slashing costs across the business and doing it in a hurry before 3G Capital with Warren Buffet, the “Sage of Omaha” arrive on the scene and peremptorily acquire you and introduce zero-based budgeting (as they have manifestly and successfully done so with KraftHeinz);

- Do the above but think big, again à la 3G Capital and merge Heinz and Kraft and, what’s more, have a go at adding Unilever into the mix to produce mega-economies of scale that astounded the market in February this year;

- Reformulate/tweak existing products and accelerate NPD to launch healthier, on-trend products. Normally, this brings a rash of kale, chia, and panoply of gluten-free ingredients, or a link with a celebrity;

- Sell under-performing divisions/categories of the business – e.g. the spreads division of Unilever (“I Can’t Believe It’s Not Butter” doesn’t have to believed, it just disappears!). This is the “shrink to success” sub-strategy (unless you’re P&G when the sale over time of its coffee, snacks and pet food businesses was an “exit food for higher margin health, beauty and homecare” strategy);

- Focus on faster-growing areas of the business. Nestlé comes to mind as it identifies – water, coffee, pet care, infant nutrition as high growth areas, with consumer healthcare a longer-term slow-burner, and accelerated pushes in emerging markets;

- Buy a big player in a fast-growing area – e.g. Danone’s purchase of White Wave for $10.4 billion, whereby a major dairy-based foods company acquires a plant-based “non-dairy dairy” company with brands such as Alpro, Horizon Organic and Silk soy milk, or Mars and its $9.1 billion purchase of pet care company VCA, Inc. in the USA (the pet care market is growing at twice the rate of consumer foods);

- Pervasively fashionable with Big Food has been the establishment of venture capital divisions with modest pots of money to buy into start-up companies that have product portfolios with high potential – e.g. Danone’s Manifesto Ventures that has invested in organic baby food start-up Yooji, Michel & Augustin (premium cookies and organic yogurts), Farmers Fridge (salad vending machines) and Accel Foods (a VC accelerator backing, inter alia, a company making tater tots from cauliflower) over the past year. Unilever, Nestlé, Kellogg’s, General Mills, Campbell’s have all been similarly busy with the hope that they’ve picked a Fever Tree start-up phenomenon that can go big time;

Campbell Soup has just announced they are joining the Plant Based Foods Association, to reinforce their commitment to healthy food and perhaps buying new brands in this area!

- Announce share buybacks to keep shareholders sweet and activist investors off the corporate back. This is a “capital structure” play that is preferred by the likes of Nestlé – and handy when one has cash but nowhere immediately to spend it on a high return opportunity;

- Finally, the far-sighted food companies place society’s interests at the centre of their businesses and communicate this effectively to consumers, shareholders and other stakeholders. Unilever and Nestlé do this best. For instance, Nestlé’s use of the Creating Shared Value (CSV) tool: focusing on areas of greatest intersection between its business and society’s concerns – products with a nutrition, health and wellness dimension perform better than junk food in the long term, rural development programmes for farmers ensure long-term ingredient supply (e.g. cocoa) and are liked by consumers who want to know who produces the ingredients for Nestlé’s KitKats, and responsible stewardship and sale of water saves costs, lives and is positive environmentally. Paul Polman, CEO of Unilever, has been a thought leader in this area – the Unilever Sustainable Living Plan is about doubling the size of its business whilst reducing its environmental footprint and increasing its positive social impact (moving towards “net positive”). Emmanuel Faber (see opening paragraph) is onside, too, launching Danone’s “One Planet One Health” signature programme.

So, is it “Big Food, Going, Going, Gone?”! Well, let’s hope it’s Big Food Bad Food heading for oblivion. But, there’s nothing wrong with big companies – they’re not intrinsically bad. They bring scale, resources, technological sophistication, jobs and, when they move in a direction that is consonant with society’s greatest needs, they can be powerful accelerators of positive change. Let’s give Big Food some encouragement and a kick up the backside and may Little Food continue to harry them mercilessly. Whether you’re Big Food or Little Food, however, the principal key to commercial success is to produce tasty products that are irresistible and produced in ways that are in tune with the values of consumers and society at large. What must stick in the craw of Big Food that has got this message is that it’s a long row to hoe! In the meantime, the most profitable companies globally in grocery are the ones pedalling cigarettes and booze. Organic yogurts and chia-coated muesli bars can be yummy but they’re not addictive. C’est la vie – it’s a cruel world!

Leave a comment