Two years ago Amazon, one of the online shopping world behemoths, confounded analysts by announcing that it was about to buy Whole Foods – an up-market bricks and mortar grocery shopping chain (June 16th, 2017). Share prices of major grocery stores plummeted, particularly in the USA (and they were rocky in the UK, too):

Grocery pundits opined that the Amazon-Whole Foods deal would change the face of grocery to the detriment of traditional supermarket players. We put in our two cents with our blog “What if …. Amazon bought Sainsbury’s?!” (July 2017). What’s more, in the aftermath of the UK regulator thwarting Sainsbury’s merger with Asda, we are minded to repeat this question!

So, has grocery retailing been turned on its head since then? No, but there’s been lots of changes. In the USA, the grocery retail giants didn’t show the white flag! Most piled into upping their online presence, not least Walmart who are bound and determined to “Out-Amazon Amazon” with initiatives such as:

- Expanding its investment in Chinese electronic marketplace company JD.Com and bringing it to the USA, alongside its own Jet.com (an acquisition in 2016 to compete with Amazon);

- Testing a grocery delivery plan – households can pay $99/year for unlimited delivery of groceries of $30+ basket size – hmm, sounds rather like Amazon Prime to us! – albeit without the music, reading material and TV freebies that’s included in Amazon prime. In the UK, Amazon hired the Top Gear guys to produce a new programme to accelerate the uptake of subscriptions.

- Substantially expanding investment in automation/AI – trialling autonomous grocery delivery, expanded robotic use in DCs.

- Selling under-performing assets (like Asda?) to generate additional funds to invest in activities that improve its competitive position against Amazon.

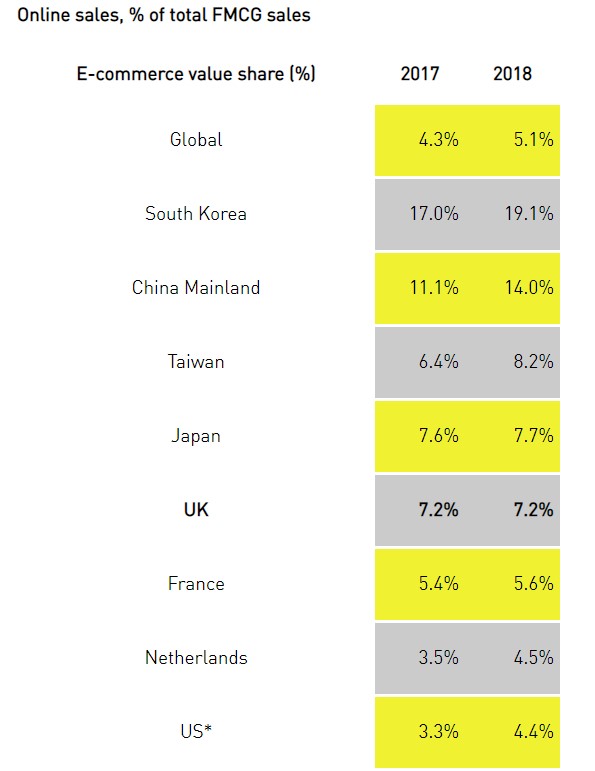

The USA has been a slow poke for online grocery shopping (3% of total grocery spend – it’s 8% in the UK) but from a low base it is growing rapidly and may reach 10% (combining delivered and click & collect) by 2024 giving the online route to the consumer a handsome value of $100 billion. Walmart’s growth in online grocery sales is much stronger than Amazon’s and for that omni-channel offer (“You can shop with us anywhere, any time, in any format”), Walmart has 10 times more stores across America than Amazon. But, they don’t have an Amazon Go offer and, mark our words, these quintessential convenience stores will be become pervasive in higher income urban markets. The real action for online grocery purchases increasingly will be in Asia. South Korea leads the global pack now, but China will dominate the online scene: Asian Millennial and Generation Z fresh food shoppers are caustic about their parents’ affection with traditional wet markets (which they see as being downright dangerous from a food safety perspective) and who would want to visit a physical store for routine food purchases in congested conurbations with scary air pollution problems?

By 2025, then, will our food shopping behaviour be radically different than it was in 2015? Yes and No! Buying food is different than, say, purchasing a branded electrical appliance, or topping up our on-hand cash, or the services of a taxi. We’d wager: you don’t have wistful moments recalling halcyon times queueing up at the bank for YOUR cash; notwithstanding your admiration for black cabs and the “The Knowledge” of their drivers, dialling up an Uber hasn’t left you in inner turmoil; and doing your research online and, then, purchasing the fridge brand of choice isn’t too difficult either. But, buying fresh foods is a different kettle of fish! Then, we’re much more contemplative.

For starters, we are conservative in what we eat – of course, there are changes but, generally, they aren’t dramatic. In history, affordability and availability were paramount and, over time, the form of the food purchased became influenced by its convenience – in contrast to now where all foods are available all of the time. Food traditions were and are important, for example, the centrality of the Sunday roast which, then, led to a cold meat meal on the Monday and a minced one of whatever remained on the Tuesday. Religion played its part – fish on a Friday to cater for Catholics and, God love The JL Partners, Waitrose continues with its “20% Off Counter Fish on a Friday”! But, keep a keen consumer eye, roast dinners, casseroles, soups and sausage-based dishes are down across the UK, and Italian, Oriental, salad and vegetarian meals are up. Potatoes are featuring in 25% less roast dinners than they were 4 years ago.

Where we purchase food changes slowly, too, reflecting not least who we trust to provide the food we feed to our families. Remind us, what experience and expertise does Amazon have in retailing fresh meat, fruit and vegetables and aren’t they a tad more complex to source than masonry drill bits? A major constraint to expanding online retail sales of fresh food in the UK and many other countries is that shoppers mistrust the retailer to select produce on the customer’s behalf – even although the likes of Sainsbury’s, hardly a Johnny-come-Lately, have been doing exactly this for 150 years!

However, the rate of change of what we eat, where we purchase and consume it is accelerating driven by, inter alia:

- Demographic change particularly in burgeoning cities – e.g. the growth of one person households (close to 50% of households in major international cities);

- Time compression for families where 2 parents are working outside the home or, even more frantic, single parent families;

- Fragmentation of the “family” meal occasioned by different working hours, proliferation of extra-curricular activities (sports, music, Ipad time, etc.);

- Increasing incidence of food allergies and dietary preferences – e.g. the 20% of families with youngsters in the 10-20 year old range who are – vegetarian or gluten-/lactose-intolerant (we refer to this as the tricky “What have you bought/cooked that Brenda can eat?” question);

- And the global impact of food trends emerging, converging and being embraced brought about by social media consumption – e.g. pervasive Instagram food pictures (David’s 9 year old granddaughter woofs down smashed avocado on sour dough toast having no truck with Fanny Craddock-esque avocado prawn cocktail with scarily pink Marie Rose sauce!);

The food service industry responding adroitly to accelerating food-to-go demand – for example:

- the likes of Pret out-performing traditional supermarkets in F2G (and buying F2G chain EAT to expand its vegetarian offer presence);

- gas/petrol stations becoming respectable places to stop by for a chocolate croissant and decent coffee (explaining why Coca-Cola swept up Costa Coffee early this year) and a nutritious, ready-to-eat salad curated by Jamie Oliver himself;

- restaurant meal delivery options arriving en masse (note that Amazon has just increased its investment in Deliveroo having failed twice to buy the company, and McDonald’s with its global link with Uber Eats is expecting a $3 bn. meal delivery business by the end of 2019);

- meal kits whisked to one’s door with the week’s meals ingredients (in the USA, Unilever increasing its investment in Sun Basket and the largest Japanese organic food investor purchasing Purple Carrot both to hold positions in vegetarian and paleo diet meal offerings).

There’s so much going on in global F2G that it makes you dizzy and the pace of change and entrepreneurial energy in the UK is frenetic!

Having taken a battering over the past few years, Big Food as we expect has come back fighting and recognised that cutting costs is not the only solution to its woes. Global brands are on the decline and regional/local ones on the up:

- Danone is focusing on growth of the local brands in its brand stable, and on high growth areas such as plant-based foods, dairy protein, rehydration (water!), and gut health (pre- and probiotics);

- Gut health has also appealed to Kellogg’s (launch of “Happy Inside” cereals) and to Unilever (investment in Culture Republick probiotic ice cream) as well as riding the healthy snacking trend by buying the UK’s Graze;

- Shifting business emphasis from slow or no growth developed markets to speedy emerging markets is the order of the day, too – Unilever’s sales increased 5% in the latter and 0.3% in the former last year;

- Even Big Meat, never first to the innovation parties, have lumbered forward with Tyson, JBS, Cargill and Purdue all launching flexitarian and plant-based “meat” products within the past few months. This is a segment that Nestlé seems stubbornly trying to embrace. Initially, the company failed with the launch of plant-based meals Garden Gourmet but, stoically Swiss as ever, Nestlé is re-launching it and has the impetus of providing its product as McDonald’s Big Vegan Burger, and has revealed to the world the Awesome Burger under the Sweet Earth label. Slow but generally sure, Nestlé aim to reach $1bn in sales within a decade from plant based products.

What’s all this mean to the rest of us – from broad acre arable farmers through SMEs in food manufacturing and meal & snack solution delivery? Change in the food and beverage industry is constant, inexorable and is clearly accelerating. Businesses of all shapes and sizes should reacquaint themselves with The Boiled Frog fable. Irrespective of the relevance to you of the second anniversary of Amazon’s Whole Foods purchase, ask yourself “In the last 24 months, what have we done in our business both to improve our position vis-á-vis our competitors and our customers?”. Go on, make a list! And for your products and services, what’s the fastest growing routes to the consumer and are you in them?

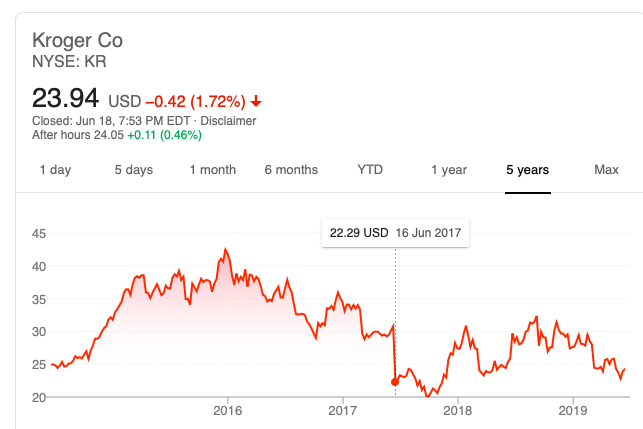

We started the blog talking about Amazon’s acquisition of Whole Foods and the tremor that this caused through global retailing. Two years on, the Whole Foods Division is the slow poke of the Amazon Empire (+2% p.a. revenue growth) dragging down overall corporate growth to a miserly 18%! Bricks & mortar grocery retailing is not in the stratospheric arena of cloud computing in which Amazon excels. Kroger – America’s Number 2 grocer – slipped backwards in sales last year. Since buying Whole Foods (and not because of), Amazon’s stock price has close to double, whilst Kroger has lurched to and fro and, currently, has scraped a 6% gain over its June 2017 price. It’s tough trucking in grocery retailing and that’s one of the reasons, dear readers, to put it delicately that big supermarket chains are such difficult entities to deal with!

[…] https://supermarketsinyourpocket.com/2019/06/26/accelerated-change-in-the-food-industry-remember-the… […]

LikeLike