One way or another, each of us ingests food every day. The intriguing question is, in the future will we be buying it from the same retail providers as in the past? Drop back a decade and the answer revolved around the perceived relentless march of the mega-supermarkets – Walmart, Tesco, Carrefour et al. Now, massively present although they are, “Big Box” retailing is looking a tad jaded, with the Germanic terrible twins, Aldi and Lidl, causing consternation and the manifestation of all that is online, Amazon, hovering menacingly! So, what’s the story?

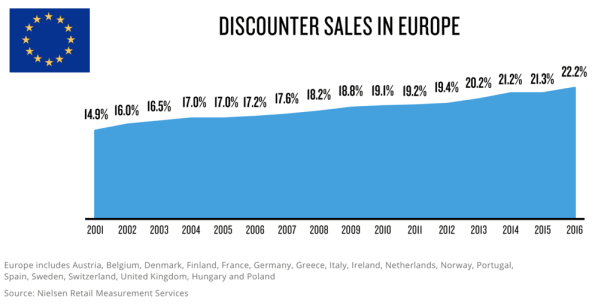

Let’s look at some facts and forecasts. In the UK, supermarkets and hypermarkets have a combined grocery market share of 55%. By 2023, their share is forecasted to slip to 52%. Let’s race ahead to 2030 – share will have dipped to the mid-40% but reports of their death will have been greatly exaggerated. Discounter share in the UK, now at 12% and expected to reach 14%+ by 2023 will nibble towards 20% by 2030. Across Europe, those pesky discounters have shown consistent ability to prosper in a hostile environment – like moths in the wardrobe, they’re very difficult to expunge!

Retail pundits are increasingly disappointed and sceptical about the future rate of growth for online grocery. In 2018, 6% of UK groceries were purchased online and this is projected to increase to a modest 8% by 2023. The disappointment is that this growth trajectory does not emulate that of hardware, electricals or fashion. We believe that in the UK online grocery share may be 15% by 2030 but what sort of groceries will be routinely sold online?

Look, there’s a big difference in the level and frequency of emotional involvement in our purchases of, say, kitchen paper towels versus meat. For paper towels, we buy our regular brand or whatever other brand is in our “paper towel repertoire”, often being influenced by whatever is on special. Few shoppers sniff the pack and search assiduously for the “best before” date! However, fresh foods are predominately supermarket labelled and we feel the need to check dates/appearance/ripeness/maybe smell because, after all, this core purchase will be eaten by me and my family. Like meat, the fruit and vegetable purchase is equally complex: green or ripened bananas?; is the avocado for guacamole tonight or do I want it to be perfectly ripe for a salad in 3 days?

Satisfying online shoppers on fresh foods is a weighty responsibility. Trust in the provider and brand owner, whether it be a supermarket or a pure online player like Ocado is paramount. So, do you think the majority of shoppers will be comfortable with their local supermarket selecting their families’ fresh foods, let alone a distanced, monolithic entity such as Amazon?! Building online share for fresh foods will be very hard work whereas doing the same for the other boring but essential stuff will be, relatively speaking, a doddle! That’s why UK online share of grocery purchases will be “only” 15% by 2030 and the disproportionate share of those online grocery purchases will be for shelf stable items that are, currently, located in the middle aisles or “the morgue” as this area is unkindly named. Surely, at least half our grocery purchases, the ones that are essential but low involvement from a shopper perspective, will be auto-replenished via signals from smart fridges and pantries in most homes within a decade?

Shoppers’ relationships with groceries have always been a bit more personal than other goods. Back in 1998, grocery sales were just 14% of total for Walmart and it took close to 20 years for “The Mother of All Grocery Retailers” to ratchet this percentage over the 50% mark (57% of Walmart’s $500 billion sales were grocery items in 2018). For Amazon, 2017 sales of $180 bn. had a tiny fresh food component – that’s one of the reasons Bezos bought Whole Foods. We’re convinced that he’s kicking himself regularly for not putting in an early bid for Sainsbury’s before they went and queered his pitch by snagging Argos and, then, Asda. Online platforms with no track record in perishable fresh foods need to earn shopper trust and an accelerated way to do this is to purchase a bricks and mortar retailer with a fresh food pedigree. The strong performance of Morrisons’ share price over the past few months is indicative that market pundits think Amazon may dip into its petty cash and fork out $8 bn. (a mere1% of its current market cap.) to buy a friendly Yorkshire grocer before the year’s out!

Pundits have a short attention span and are impatient by nature. Amazon takes a longer-term view. David signed up as a customer with Amazon in 1998 – 20 years ago, when Bezos was just moving out of his garage using it as an office and depot and his “books by mail” business was taking off. In 2018, Amazon has a 40% share of ALL online sales in the USA. Are its sales peaking? Hardly! 85% of retail in America is still bricks and mortar-based. But Bezos believes that Amazon must expand and grocery sales are an integral part of this expansion. Look to China for endorsement – both Jack Ma (Alibaba) and Pony Ma (Tencent) are expanding their internet-based businesses by buying into traditional supermarket chains.

China’s level of digitalisation is enough to make Western online companies dribble with excitement. Payment by touch phone dominates and cash is passé. B2C e-commerce penetration in China far exceeds that in any other market in the world. Are the Chinese more tech-savvy? No – they’re leap-frogging traditional stores because of poor store networks and shocking product availability. For a US food producer, partnering with the top 4 grocers gives you access to half of the US food market. In China, by contrast, the top 4 grocers connect you with 5.7% of food retail spending (The Economist Intelligence Unit). This is a headache for food producers and consumers alike – supply chains are long, circuitous and, often, dodgy. So many Chinese consumers shop online because the products they want are not available offline and, as a bonus, they don’t have to sit in a horrendous traffic jam going to and from the store!

Getting back to our food purchasing behaviour – let’s not forget that whilst food is fuel, it’s also for some occasions (which are being squeezed) hugely social, fun, family, tradition, entertainment, reward and much more. Online is great for basics but can be at odds with consumer values when we are in feasting rather than refuelling mode. Yes, we can make “Mindful Choices” shopping online but it’s more rewarding when we have an opportunity to interact with the physical food and those that sell it. Capturing online share of fresh foods and story foods will be a marathon not a sprint. But focussing on the battle solely for grocery market share is profoundly blinkered. The overall market for food must be viewed in the round. What about food consumed out-of-home or when we “eat out in” using the likes of deliveroo, uber eats, etc.?

The food-to-go market is huge and growing substantially faster (x2) than traditional grocery. Whereas supermarkets are expanding their food-to-go offer, they are not the movers and shakers. 60% of this market is taken by specialists and by QSR, but over the next 5 years the specialists will advance at pace and QSR overall will struggle, as some fail to keep pace with the digital/technological initiatives of the global fast food employers (particularly McDonald’s who have done remarkably well in the UK during a torridly competitive period for food service). For best in class, look to Pret (snapped up recently by Germany’s JAB), Itsu and, as ever, M&S’s food-to-go offer can be fabulous. Younger consumers are the driving force in food-to-go and when they want it, they want it NOW, not in a minute but NOW! Desperate to claw their share of this market, supermarkets are and will continue to revert to type and rely on astonishingly low-priced meal deals. It’s in their DNA to foment a “race to the bottom” on price.

As traditional eating patterns (breakfast-lunch-evening meal) break down and are replaced by a series of mini-meals and/or snacks which can be bought and eaten out, or delivered in to office or home, demand for old-fashioned food ingredients wanes. Breakfast is purchased on the way to work, lunch is at or close to place of work, dinner is carried home or “ubered-in”. The result is that the pre-eminence of the supermarket as a destination to purchase food is lessened substantially. In short, the meal/snack market moves from being highly competitive to, let’s call it, ubercompetitive!

Is this good news? Well, YES from a consumer perspective with a myriad of food businesses vying for our attention and opportunities galore for those that are quick on their feet, technologically adept and are well tuned-in to fast-changing consumer whims and fancies. But, it’s more challenging for monolithic 20 Century grocery retailers who may lose sales massively from the core of their stores to pure play online merchants and struggle to keep up in the fast-changing world of food on the move! Surely, it’s good news for food suppliers as new routes to the consumer emerge and become established and, in doing so, take share of stomach from the traditional supermarkets. So, do we expect to see tumbleweed blowing through dust-covered aisles of abandoned Tesco and Sainsburys/Asda supermarkets? No – they have huge areas of strength including a thorough understanding of sourcing fresh foods, the capacity and resources to change, and the capability to be world class omni-channel retailers.