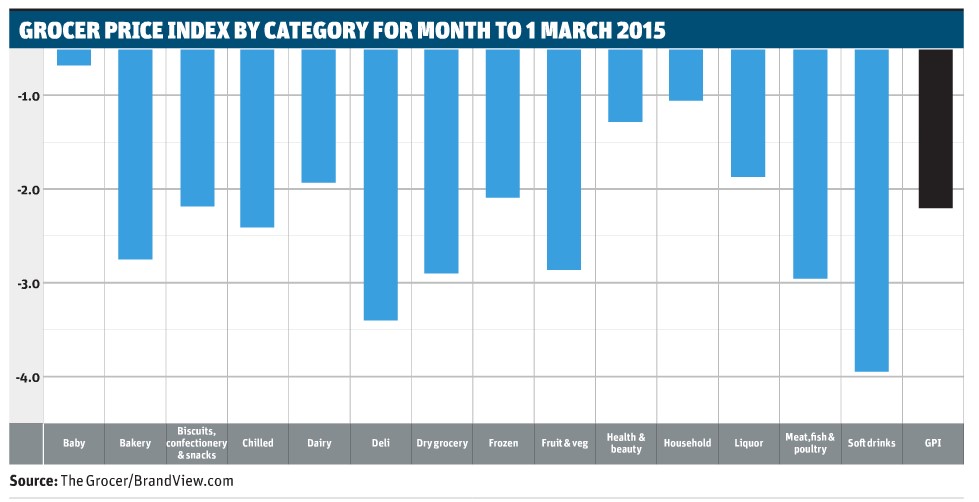

This month in the UK, the inflation rate dropped to 0%, a level not seen for 50 years and, what’s more, we could see negative figures (deflation) in the upcoming months. The principal drivers are declines in both fuel and grocery prices: in February, every major grocery category experienced month on month value falls (see chart) – a month in which, historically, price increases are expected particularly for fresh produce. Surely, this is good news for consumers but has dire consequences for the major supermarket retailers who are caught by a double whammy blow – lower prices on lower volumes of groceries with excruciating negative impact on their net margins; and continuing relentless erosion of their market shares by the hard discounters with Aldi and Lidl currently holding about 8% national grocery market share but forecasted to grow to 15% over the next very few years.

By European standards, the British economy is in good shape: unemployment falling to about 6% (in Spain it’s 23%!); and real household incomes are increasing as we claw our way out of austerity Britain. Will shoppers splash out and increase their weekly grocery shopping? Probably not and for two reasons: first, after a 7 year hard slog, they’ll be looking to buy that overdue new furniture or appliance or, maybe, reward the family with a sun-drenched holiday; and, secondly, grocery retailers are bribing their customers to stick with them/switch allegiance by offering ever lower prices! Asda, the price leader for supermarkets, is investing £300 million this year in lower prices, part of a £1 billion programme over the next five years. Tesco is slashing sku numbers to simplify its offer and reduce costs. Yet, still, there is a significant gap in prices between the big boys and the hard discounters and the so-called retail theatre in “The Big Sheds” of Asda/Tesco etc. (e.g. fancy coffee shops, restaurants, take out food concessions) are insufficient to woo shoppers away from limited assortment discounters. What’s more, the stature of Aldi and Lidl continues to grow: Aldi announcing that it is the first retail partner for the UK Olympic team for Brazil; and Lidl with its award-winning premium own label products stealing the show from the supermarkets.

In short, it looks a very tough journey for “traditional” supermarkets over the next couple of years: on-line growth will reduce volume through the big stores; as will volume losses at the margin to convenience stores; hard discount and pound store pressure will be inexorable; and savvy shoppers will get even savvier in an increasingly transparent and multi-channel market environment. We may see a slimming down of grocery retail players in the UK market. Fingers crossed that zero inflation doesn’t drift down into morbid deflation (Japanese-style stagflation) where shoppers hold off big ticket purchases in anticipation of even lower prices to come! But, hey, let’s end on an upbeat note. In the UK, our population is increasing (whereas it’s declining in Germany/Spain/Italy), household incomes are growing again, interest in food and where it comes from is on the up, and consumers are willing and able to reward grocery industry players who deliver on grocery price/quality values and social values. Onwards!

Source The Grocer

Leave a comment